Florida has some of the most layered medical billing regulations in the country. The state combines its own statutes on balance billing, price transparency, and debt collection with federal rules like the No Surprises Act and HIPAA. For providers, missing even one requirement can lead to fines or denied claims.

The stakes are real. Roughly 1.5 million Floridians report owing medical bills each year, according to Florida Daily. At the same time, Medical Billing Advocates of America reports that up to 80% of medical bills contain at least one error. These numbers make it clear why understanding the laws behind every bill matters.

This guide breaks down every Florida law that directly affects medical billing. You will find the specific statutes, their real-world impact, and the steps to stay compliant. We also cover the latest changes, including SB 1808 and the Live Healthy Act, that took effect in 2025 and 2026.

What Florida Laws Govern Surprise and Balance Billing?

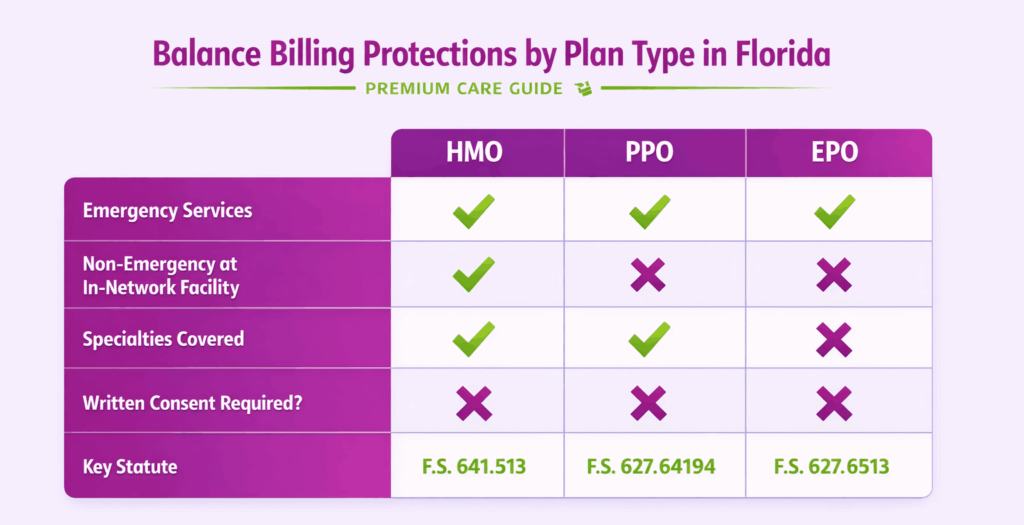

Florida has strong protections against surprise and balance billing. These rules apply to both emergency and non-emergency settings, and they cover patients enrolled in HMO, PPO, and EPO plans licensed in the state. To navigate these complexities seamlessly, many high-performing practices utilize medical billing services in Florida to ensure every claim is optimized for both state compliance and maximum reimbursement.

What Is Balance Billing Under Florida Law?

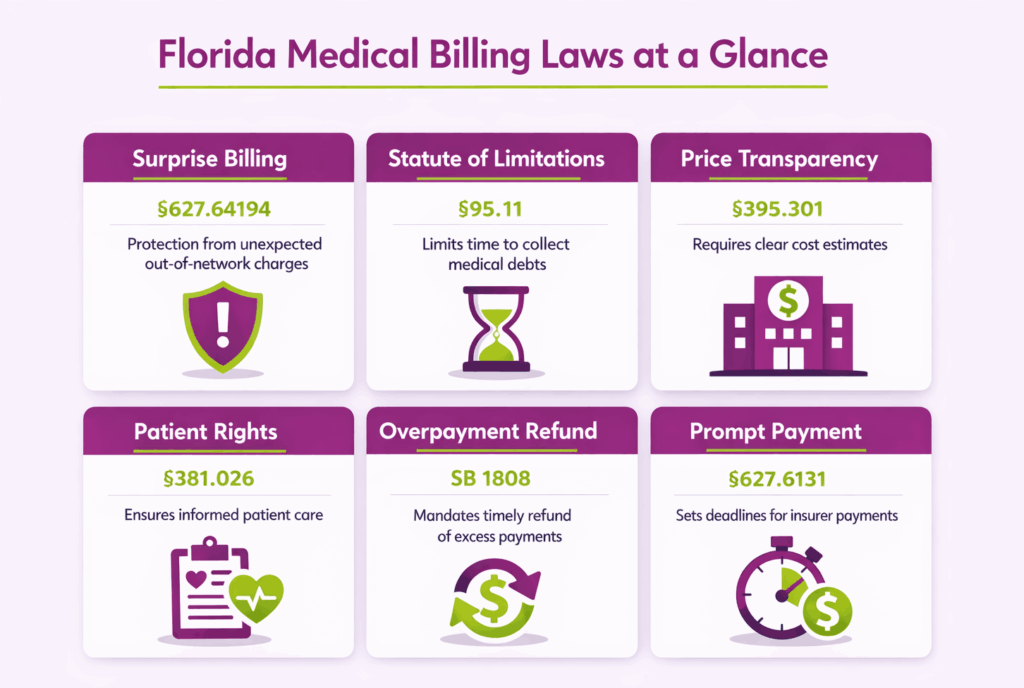

Balance billing happens when an out-of-network provider bills a patient for the difference between the provider’s full charge and what the insurance plan paid. Florida law restricts this practice under two key statutes. Section 627.64194 covers patients in PPO and EPO plans. Section 641.3154 covers HMO members. Together, these laws limit what patients owe to their in-network cost-sharing amounts like copays, coinsurance, and deductibles.

You can learn more about what balance billing is under Florida law in our detailed guide.

How Does Florida’s Surprise Billing Law Protect Patients in Emergency Settings?

Florida law bars out-of-network providers from balance billing patients for emergency services. This applies to all commercially insured patients enrolled in HMO, PPO, or EPO plans licensed in Florida. The patient only pays their in-network cost-sharing amount. The insurer is responsible for paying the provider directly.

This protection extends to post-stabilization services as well, unless the patient gives written consent to waive their rights. Providers cannot pressure patients into signing that waiver.

What Are the Balance Billing Rules for Non-Emergency Services at In-Network Facilities?

When a patient receives non-emergency care at an in-network hospital or ambulatory surgical center, out-of-network providers at that facility cannot balance bill the patient. This rule covers specific specialties: emergency medicine, anesthesia, pathology, radiology, laboratory, neonatology, assistant surgeons, hospitalists, and intensivists.

For HMO members, Florida goes further. Section 641.3154 prohibits all balance billing by out-of-network providers, even in non-emergency settings. PPO members are protected when they do not have the ability or opportunity to choose an in-network provider at the facility.

For any other out-of-network services at in-network facilities, a provider can only balance bill the patient if the patient signs a written consent form giving up their protections.

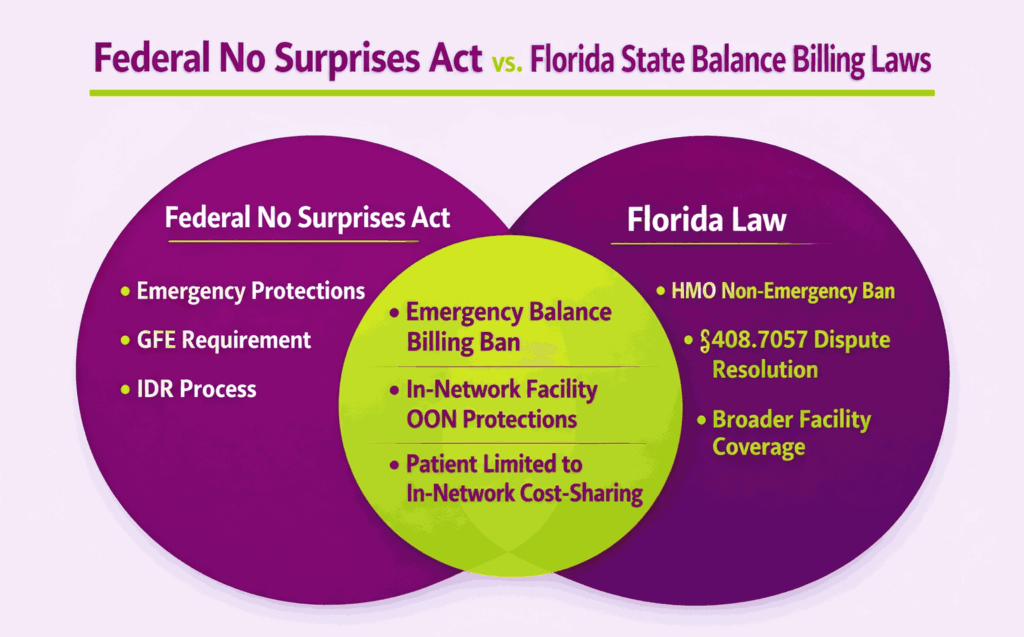

How Does the Federal No Surprises Act Interact With Florida’s Balance Billing Laws?

The federal No Surprises Act (NSA), effective January 2022, set a national floor for surprise billing protections. Florida’s state laws existed before the NSA and remain active because they offer broader coverage in several areas.

The biggest difference is HMO protections. The NSA does not specifically address HMO balance billing in non-emergency settings. Florida law does, through Section 641.3154. Florida also has its own dispute resolution framework under Section 408.7057, which runs alongside the federal independent dispute resolution (IDR) process.

Providers operating in Florida must comply with both layers. When Florida law gives the patient greater protection, state law controls.

What Is the Dispute Resolution Process for Balance Billing in Florida?

If a provider and an insurer cannot agree on payment for out-of-network services, Florida law provides a consumer dispute resolution process under Section 408.7057. Either party can initiate it. The dispute resolution organization reviews the evidence and issues a finding.

Florida law also requires this process to be transparent. The organization must publish the evidence and data it used to reach its decision. This gives both providers and payers a clear record to reference for future billing disputes.

What Are the Statute of Limitations and Billing Timelines in Florida?

Florida has multiple timelines that control how long providers can bill patients and how long creditors can pursue medical debt. These timelines vary based on the type of facility, the payer contract, and whether the debt involves a licensed facility.

How Long Can a Doctor Bill You After Service in Florida?

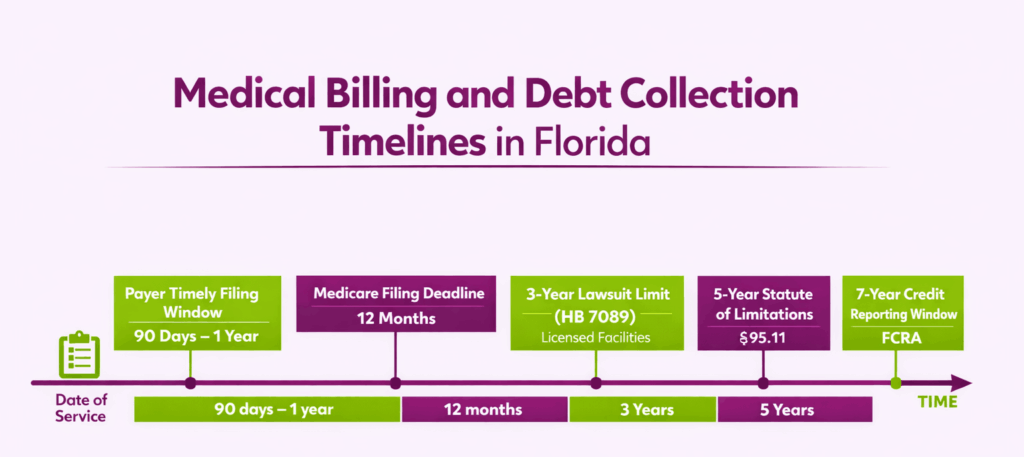

Under Florida Statute Section 95.11(2)(b), the general statute of limitations on a written contract is five years. Most medical bills fall under this category. This means a provider can send you a bill for services rendered up to five years after the date of service.

However, insurance contracts often set much shorter time limits for filing. Most commercial payers require claims within 90 days to one year. Medicare requires submission within 12 months of the date of service. Florida Medicaid deadlines vary by managed care plan contract. If a provider misses the payer’s filing window, the claim gets denied, but the patient may still be responsible depending on the circumstances.

What Is the 3-Year Statute of Limitations for Licensed Facility Medical Debt?

The Live Healthy Act (HB 7089), signed into law in 2024 and effective October 1, 2024, introduced a shorter collection window for licensed facilities. Hospitals and ambulatory surgical centers now have a three-year statute of limitations for legal action to collect medical debt.

This is a significant reduction from the previous five-year window. The law also added personal property exemptions from legal process for medical debts originating from licensed facilities. It requires these facilities to post consumer-friendly lists of standard charges on their websites and establish internal grievance processes for patients to dispute charges.

Note that the three-year limit applies specifically to debt collection lawsuits filed by licensed facilities. Independent physicians and other non-facility providers still operate under the general five-year statute.

Can a Doctor Bill You 2 Years Later in Florida?

Yes, as two years falls well within both the three-year window for licensed facilities and the five-year window for other providers. A provider billing you at the two-year mark is fully within their legal rights.

That said, if the provider’s insurance contract had a shorter timely filing deadline and the provider missed it, the payer may deny the claim. In that situation, whether the patient is liable for the balance depends on the specific contract terms and the circumstances of the delay.

What Happens When the Statute of Limitations Expires on Medical Debt in Florida?

Once the statute of limitations passes, the debt becomes “time-barred.” This means the creditor can no longer file a lawsuit to collect it. However, the debt itself does not disappear. The provider or collection agency can still contact you and request payment. They just cannot sue you or threaten legal action.

Under both the federal Fair Debt Collection Practices Act (FDCPA) and the Florida Consumer Collection Practices Act (FCCPA), collectors who threaten lawsuits on time-barred debt are violating the law. Patients can pursue statutory damages of up to $1,000 for such violations.

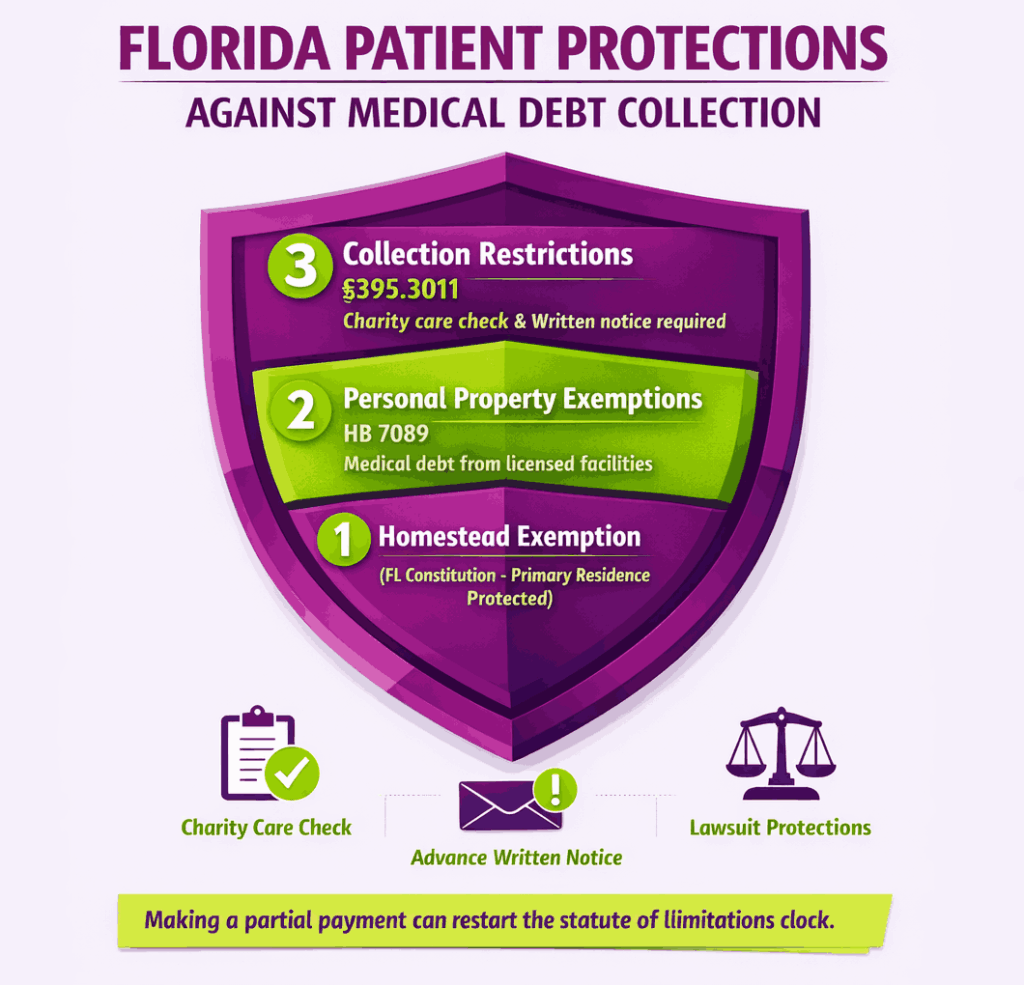

One critical risk for patients: making even a small partial payment on time-barred debt can restart the statute of limitations clock. This resets the creditor’s ability to sue. Patients should consult legal counsel before making any payment on old medical debt.

What Are the Price Transparency and Good Faith Estimate Requirements in Florida?

Florida requires healthcare facilities to give patients clear pricing information before and after treatment. These rules come from both state statute and federal law, and they apply differently depending on the facility type and the patient’s insurance status.

What Does Florida Law Require for Price Transparency?

Section 395.301 of the Florida Statutes requires licensed facilities to publish pricing information on their websites. This includes payment data for defined bundles of services and procedures. The Live Healthy Act expanded this requirement, mandating that hospitals post a consumer-friendly list of standard charges for shoppable healthcare services.

Ambulatory surgical centers received a delayed timeline. The shoppable services requirement does not apply to ASCs until January 1, 2026. Facilities that fail to comply face potential enforcement action from the Agency for Health Care Administration (AHCA).

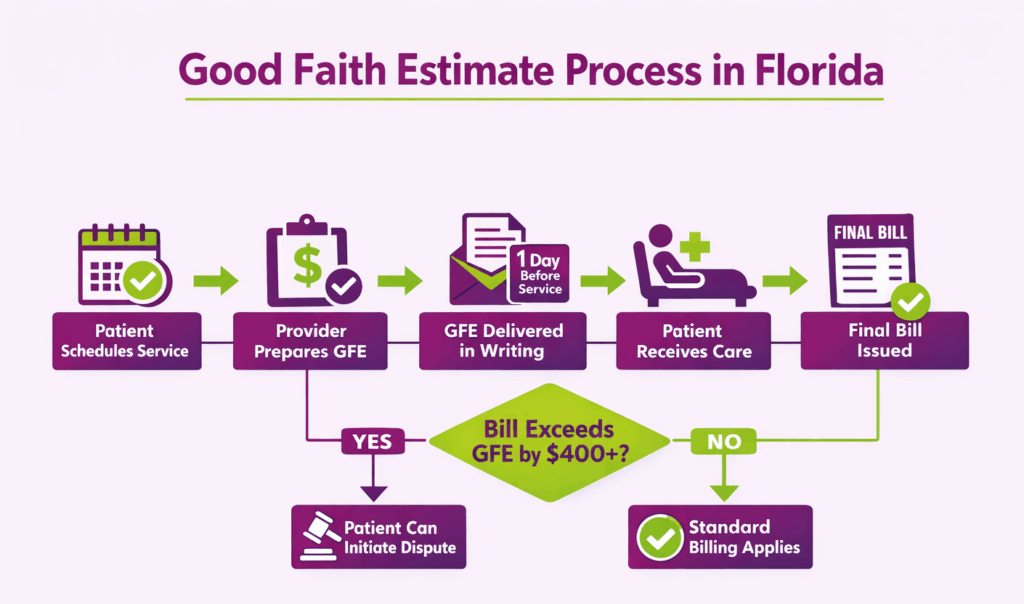

What Is a Good Faith Estimate Under Florida and Federal Law?

The federal No Surprises Act requires providers to give uninsured and self-pay patients a written Good Faith Estimate (GFE) of expected charges. This estimate must be provided at least one business day before a scheduled service. Patients can also request a GFE before scheduling.

The GFE must cover the total expected cost, including related charges like medical tests, prescription drugs, equipment, and hospital fees. If the final bill exceeds the GFE by $400 or more, the patient has the right to dispute the bill through the federal patient-provider dispute resolution process.

Florida updated Section 395.301 to align with and build on these federal GFE provisions. However, certain state-level GFE changes are contingent on HHS, the Department of Labor, and the Department of the Treasury issuing a final rule on good faith estimates under the Public Health Services Act. AHCA will notify providers when that trigger is met.

What Must Be Included in an Itemized Patient Statement in Florida?

Section 395.301 sets specific requirements for every itemized bill a licensed facility issues. Each statement must prominently display the telephone number of the facility’s patient liaison responsible for resolving billing disputes.

The facility must also make all records necessary for verifying the accuracy of a bill available to the patient within 10 business days of the request. If a patient is placed on observation status instead of inpatient status, the facility must document this in the discharge papers and notify the patient accordingly. This distinction matters because observation status can significantly change the patient’s financial responsibility for the visit.

What Are Patient Billing Rights Under Florida Law?

Florida gives patients a specific set of billing-related rights under state statute. These rights are enforceable, and providers are required to make patients aware of them. Understanding these rights also matters for providers, because violations can trigger complaints and regulatory action.

What Does the Florida Patient’s Bill of Rights Say About Billing?

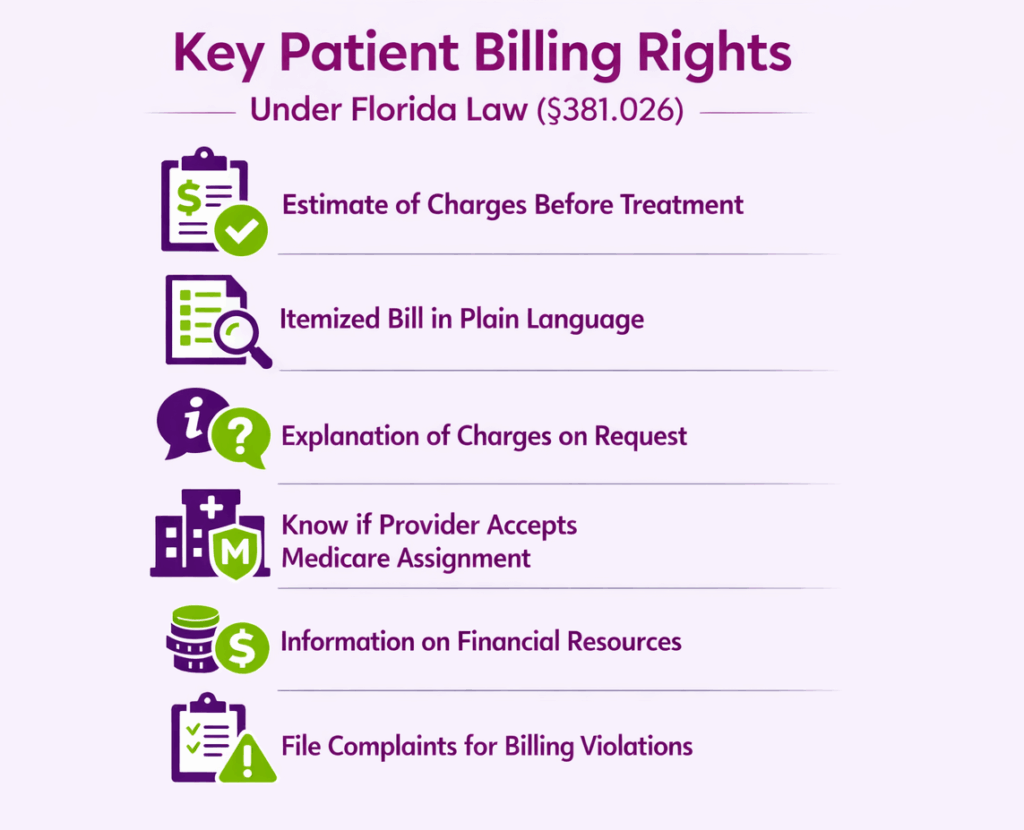

Section 381.026, known as the Florida Patient’s Bill of Rights and Responsibilities, requires every healthcare provider and facility to recognize specific patient rights during care. Several of these rights directly affect billing.

Patients have the right to receive a reasonable estimate of charges before treatment. They can request and receive a copy of an itemized bill written in understandable language. If anything on that bill is unclear, the patient can ask for an explanation, and the provider must respond. Patients also have the right to know whether their provider accepts the Medicare assignment rate and to receive full information about available financial resources for their care.

Florida law requires facilities to post a summary of these rights where patients can see them. Providers must also make the full text of the law available on request.

What Are Patient Responsibilities Under Florida Billing Law?

Section 381.026 is not one-sided. It also outlines patient responsibilities that affect billing disputes and outcomes. Patients are expected to understand the terms of their insurance coverage and approved providers. They are responsible for providing accurate personal and insurance information, following through on financial obligations, and notifying providers when they cannot keep appointments.

These responsibilities matter in billing disputes. A patient who did not verify their coverage or provide correct insurance details may have limited grounds to challenge a resulting balance. Providers can reference these statutory responsibilities when responding to billing complaints.

How Can Patients File Billing Complaints in Florida?

Florida has multiple channels for billing complaints, and the right agency depends on the nature of the issue.

For insurance-related billing disputes, patients can file with the Florida Department of Financial Services, Division of Consumer Services. For complaints against a licensed healthcare facility’s billing practices, the Agency for Health Care Administration (AHCA) handles investigations through its Florida Health Care Complaint Portal. For complaints against individual practitioners, the Florida Department of Health accepts filings through its enforcement division. Complaints must be submitted in writing, and the practitioner receives a copy if an investigation is opened.

For issues that fall under the federal No Surprises Act, patients can also contact the CMS No Surprises Help Desk at 1-800-985-3059 or visit cms.gov/nosurprises.

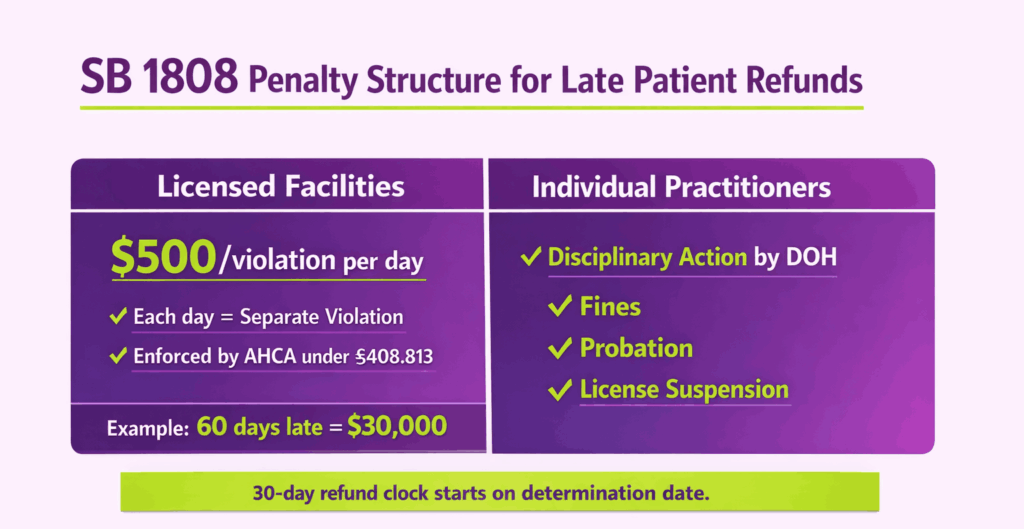

What is Florida’s Patient Overpayment Refund Law (SB 1808)?

This is one of the newest and most impactful billing laws in Florida. SB 1808 went into effect on January 1, 2026, and it creates a hard deadline for providers to return money that patients overpaid. The penalties for non-compliance are steep.

What Does SB 1808 Require Providers to Do?

Under SB 1808, licensed healthcare facilities and practitioners must refund any patient overpayment within 30 days of determining that the overpayment occurred. An overpayment happens when a patient pays more than the final billed amount after adjustments, insurer reimbursements, or negotiated discounts. Common triggers include duplicate charges, coding errors, and retroactive insurance adjustments.

The law applies when the provider has submitted a claim for reimbursement to a government program like Medicare or Medicaid, a private health insurer, or an HMO. It does not apply to overpayments made by insurers to providers, which are already covered under existing Florida insurance law. It also does not cover payments for services that were never billed to an insurer, such as self-pay or uninsured patient payments for non-covered services.

What Are the Penalties for Not Refunding Patient Overpayments in Florida?

The consequences differ based on the provider type. For licensed facilities regulated by AHCA, each day that a refund remains outstanding counts as a separate violation under Section 408.813. Fines can reach up to $500 per violation per day. That adds up fast. A single unresolved overpayment held for 60 days past the deadline could result in a $30,000 fine.

For individual practitioners, non-compliance constitutes grounds for disciplinary action under Florida’s professional licensing regulations. This can include fines, mandatory corrective action, probation, or license suspension. The Florida Department of Health oversees enforcement for practitioners.

How Should Providers Update Their Billing Processes for SB 1808?

Forward-thinking providers often partner with top medical billing companies in Florida to implement automated detection systems that turn compliance requirements into streamlined, professional workflows. This means running regular payment audits, cross-referencing patient payments against final adjudicated amounts, and flagging accounts where insurance paid after the patient already settled the balance.

Once an overpayment is identified, the determination date must be documented. That date starts the 30-day clock. Billing teams should have a standard refund workflow that includes a written notification to the patient explaining the overpayment amount and the refund. Every step should be documented to defend against potential complaints or audits.

Providers who outsource billing should confirm that their RCM partner has updated workflows specifically for SB 1808 compliance. The liability stays with the licensed provider, not the billing company.

What Are the Insurance Claim Filing and Prompt Payment Rules in Florida?

Florida has specific rules that govern how quickly insurers must process claims and how quickly providers must submit them. These timelines protect both sides. Providers get paid faster, and patients avoid being caught in the middle of slow billing cycles.

What Does Florida’s Prompt Payment Law Require?

Section 627.6131 is Florida’s prompt payment statute for health insurers. It sets clear deadlines for insurers to either pay or deny a clean claim. A clean claim is one submitted with all mandatory data fields completed, using the standard HCFA 1500 format for non-institutional providers or the UB-92 format for institutional providers.

When an insurer fails to pay a clean claim within the statutory deadline, the provider is entitled to interest on the overdue amount. The law also prohibits insurers from using claim processing delays as a tactic to avoid payment. If an insurer denies or contests a claim, it must provide a clear explanation of the reason.

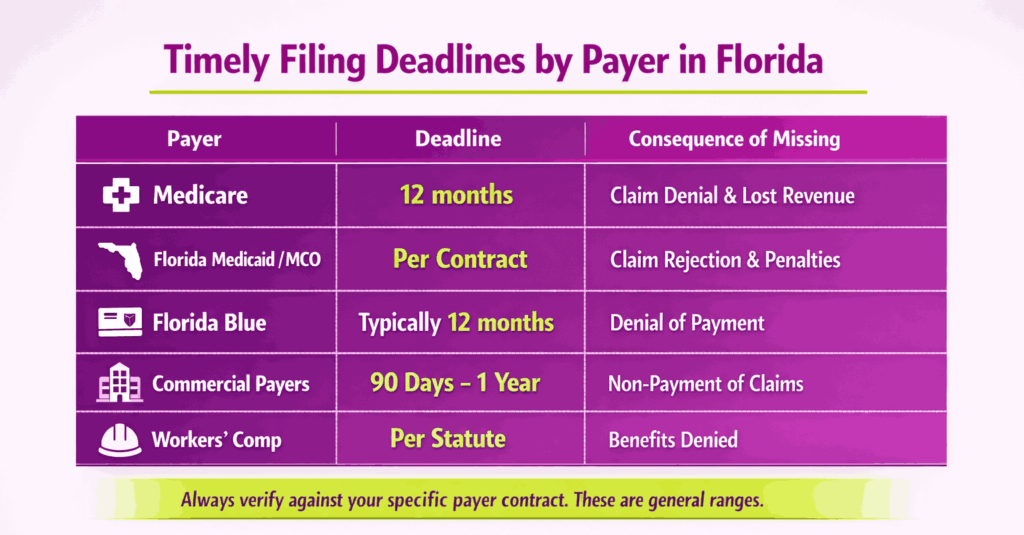

What Are the Timely Filing Deadlines for Insurance Claims in Florida?

Timely filing deadlines are set by each payer, not by a single state statute. However, Florida law creates the outer boundaries. Most commercial payers in Florida require claims within 90 days to one year from the date of service. Medicare’s national deadline is 12 months. Florida Medicaid deadlines depend on the specific managed care organization contract and AHCA rules.

Missing a timely filing deadline is one of the most common and preventable causes of lost revenue. These denials are almost never overturned on appeal unless the provider can prove extraordinary circumstances. Tracking filing deadlines by payer and automating submission workflows is essential for any Florida practice.

What Protections Do Providers Have Against Improper Billing Investigations?

Section 627.6131 also protects providers during billing disputes. When a patient notifies their insurer in writing of a potential improper billing, the insurer must investigate. If the insurer finds that the patient was billed for services they did not receive, it must notify both parties and reduce the payment to the provider accordingly.

During this process, the provider is restricted from collecting from the patient. Section 627.6131(9) states that a provider cannot pursue payment from the patient, take legal action, or report the debt to a credit agency while a claim dispute is pending. This protection lasts through the insurer’s internal dispute resolution process, up to a maximum of 60 days. Copays, coinsurance, and deductibles owed by the patient are exempt from this restriction.

How Do HIPAA and Florida Privacy Laws Affect Medical Billing?

HIPAA sets the federal baseline for protecting patient health information in billing. But Florida has its own privacy statutes that go further in several areas. Providers operating in Florida must comply with both, and the stricter rule always wins.

Where Does Florida Law Differ From or Preempt Federal HIPAA?

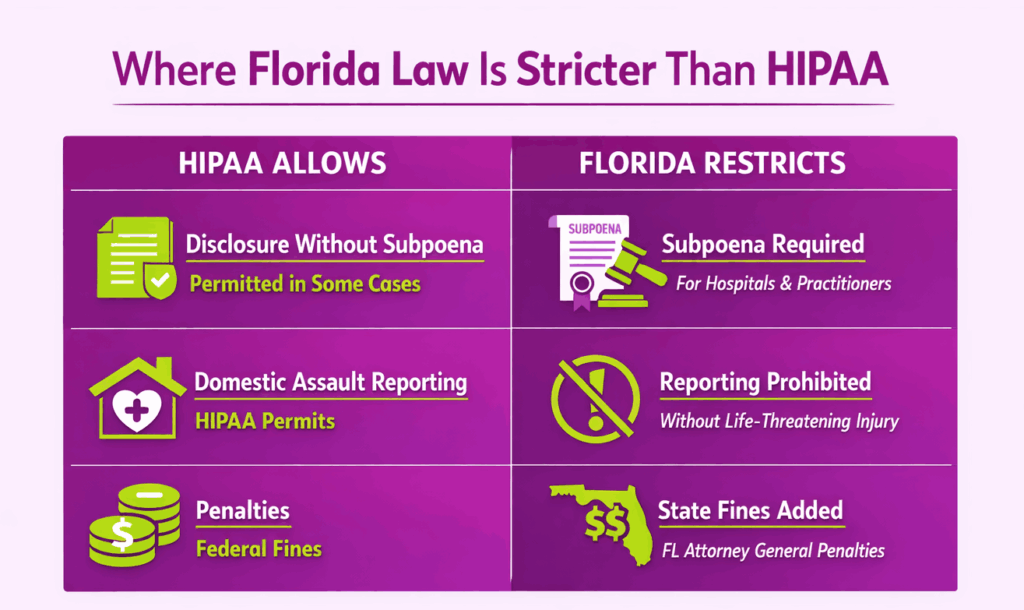

HIPAA permits certain disclosures of protected health information (PHI) without patient authorization in specific situations, such as law enforcement requests and public health reporting. Florida law is more restrictive in several of these cases.

Section 395.3025 prohibits hospitals from disclosing patient information in circumstances where HIPAA would allow it, unless a subpoena is presented. Section 456.057 applies the same restriction to independent healthcare practitioners. This means a Florida provider cannot rely on HIPAA’s broader disclosure permissions alone. They must check whether Florida law imposes a tighter standard first.

Florida’s mandatory reporting rules also diverge from HIPAA. Sexual battery, child abuse, and sexual abuse of a patient by hospital staff must be reported. But suspected domestic assault without life-threatening injuries must not be disclosed, even though HIPAA would permit it. Getting this wrong exposes the provider to state-level penalties on top of any federal consequences.

What Are the HIPAA Compliance Requirements Specific to Medical Billing in Florida?

Every Florida provider that submits electronic claims must comply with HIPAA’s Transaction and Code Sets Rule under Part 162. This includes using correct National Provider Identifiers (NPIs) in eligibility checks, authorization requests, and claims submissions. Incorrect NPIs cause claim rejections and payment delays.

Providers must also ensure that all billing data containing PHI is protected under the HIPAA Security Rule. This covers electronic claims, patient statements, Explanation of Benefits documents, and any billing records stored or transmitted digitally. Any third party handling billing data, whether an RCM company, clearinghouse, or IT vendor, must have a signed Business Associate Agreement in place before accessing PHI.

What Penalties Do Florida Providers Face for HIPAA Violations in Billing?

Federal HIPAA penalties follow a four-tier structure based on the level of negligence. Fines range from $145 per violation for unknowing breaches up to $2,190,294 per violation for willful neglect. Criminal penalties can reach $250,000 in fines and up to 10 years imprisonment for intentional misuse of PHI.

Florida adds another layer. The state Attorney General can enforce consumer protection violations related to PHI breaches under the Florida Deceptive and Unfair Trade Practices Act. These state-level penalties are separate from and in addition to federal fines. In 2025, BayCare Health System in Florida paid an $800,000 settlement to the federal Office for Civil Rights after an employee accessed patient records without authorization. That case also triggered a two-year corrective action and monitoring plan.

The takeaway for providers: a single billing-related HIPAA violation in Florida can result in penalties from both federal and state authorities simultaneously.

What Are the Florida Medicaid and AHCA Billing Requirements?

Florida’s Medicaid program is administered by the Agency for Health Care Administration (AHCA). Providers who bill Medicaid must follow AHCA’s specific rules on enrollment, coding, claim submission, and reimbursement. These rules operate on top of federal Medicaid requirements and carry their own enforcement mechanisms.

What Billing Rules Does AHCA Set for Florida Medicaid Providers?

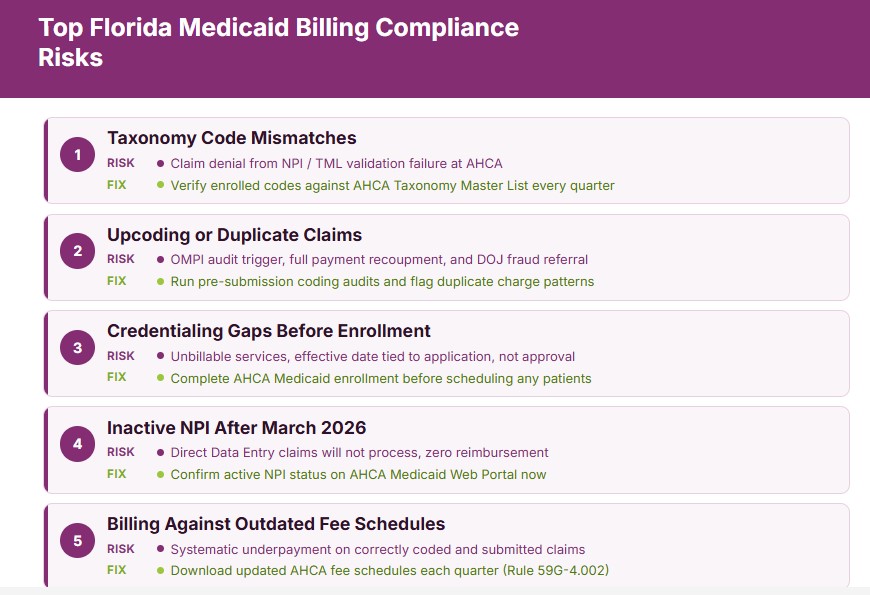

AHCA governs Medicaid reimbursement through Rule 59G-4.002, which sets provider reimbursement schedules and billing codes. Fee schedules are updated throughout the year, and billing against outdated schedules is a common cause of underpayment and claim denials.

Most Florida Medicaid members are now enrolled in managed care plans under the Statewide Medicaid Managed Care (SMMC) program. AHCA launched SMMC 3.0 in February 2025, which introduced regionally tailored plans, stricter quality performance metrics, and performance-based reimbursement structures. Providers billing under SMMC 3.0 must align their documentation and coding with these updated quality standards or risk reduced payments and increased audit exposure.

AHCA also maintains the Taxonomy Master List (TML), which maps provider types and specialty codes used in claims processing. Claims are validated against a provider’s enrolled taxonomy and NPI. A mismatch between the taxonomy on file and the taxonomy submitted on a claim will trigger a denial.

What Are Common Medicaid Billing Compliance Risks in Florida?

Several billing errors consistently put Florida Medicaid providers at risk. Duplicate claims, upcoding, and billing for undocumented services are the fastest paths to an audit. AHCA’s Office of Medicaid Program Integrity (OMPI) actively monitors claims data for these patterns.

Credentialing gaps are another major risk. Providers who begin seeing Medicaid patients before their enrollment is confirmed with AHCA cannot bill retroactively for those services. Florida Medicaid ties the effective billing date to the application submission date, not the approval date. A clean application submitted on day one gives you that effective date. A rejected application that gets resubmitted two months later costs you two months of unbillable services.

AHCA is also launching a completely new Medicaid enrollment system in April 2026. Providers with inactive portal accounts or outdated enrollment data risk disruption during the migration. Additionally, CMS set a March 27, 2026, NPI enforcement deadline. Claims submitted via Direct Data Entry without an active NPI on file will not process.

What Are the Penalties for Florida Medicaid Billing Violations?

AHCA can impose administrative fines on facilities for billing violations under Section 408.813. OMPI can recoup overpayments directly from providers and refer cases involving suspected fraud to the Department of Justice for prosecution under the False Claims Act.

For individual practitioners, Medicaid billing violations can trigger disciplinary action through the Florida Department of Health. Penalties include fines, mandatory corrective action plans, probation, and license suspension or revocation. In fraud cases, criminal prosecution can result in exclusion from all federal healthcare programs, which effectively ends a provider’s ability to practice.

What Are the Medical Debt Collection Laws in Florida?

Florida regulates how medical debt can be collected through a combination of state and federal law. These rules set boundaries on what collectors can do, how long debt stays actionable, and what patient assets are protected. Providers who also handle collections internally need to follow the same rules that apply to third-party agencies.

What Rules Must Debt Collectors Follow When Collecting Medical Debt in Florida?

Two laws govern debt collection behavior in Florida. The federal Fair Debt Collection Practices Act (FDCPA) applies to third-party collectors. The Florida Consumer Collection Practices Act (FCCPA) applies to both third-party collectors and original creditors, giving it a broader reach than federal law.

Both laws prohibit misrepresenting the legal status of a debt, using deceptive or abusive tactics, and threatening legal action on debt that is past the statute of limitations. Collectors must provide written verification of the debt upon request, including the original creditor and the amount owed. Violations can result in statutory damages of up to $1,000 per incident under the FDCPA, plus actual damages and attorney’s fees.

Florida also enacted Section 395.3011 in 2024, which specifically regulates extraordinary collection actions by hospitals and ASCs. These facilities cannot sue a patient, sell the debt, report it to credit agencies, or take other aggressive collection steps without first making reasonable efforts to determine if the patient qualifies for charity care and providing advance written notice.

How Does Medical Debt Affect Credit Reports in Florida?

Under the Fair Credit Reporting Act (FCRA), most negative information, including delinquent medical debt, can remain on a credit report for seven years from the date of first delinquency. This timeline is separate from the statute of limitations on the debt itself.

The CFPB issued a rule in January 2025 that would have banned medical debt from credit reports entirely. However, the rule’s implementation has faced legal and political challenges. Providers and patients should monitor the status of this rule rather than assume it is in effect.

One important detail: hospitals typically do not report directly to credit bureaus. The reporting usually happens after the debt is sold or sent to a third-party collection agency. Under Section 395.3011, Florida facilities that sell medical debt must have a contract requiring the buyer not to charge interest or fees beyond the original amount and to return the debt if the patient qualifies for charity care.

What Exemptions Protect Patients From Medical Debt Collection in Florida?

Florida provides several asset protections for patients facing medical debt collection. The Florida Constitution exempts a debtor’s primary residence (homestead) from most creditor claims, including medical debt judgments. This is one of the strongest homestead protections in the country.

The Live Healthy Act (HB 7089) added personal property exemptions specifically for medical debt arising from services at licensed facilities. These exemptions sit on top of the existing statutory protections under Chapter 222 of the Florida Statutes, which cover items like wages, retirement accounts, and certain personal property up to defined limits.

How Can Healthcare Providers Stay Compliant With Florida Medical Billing Laws?

Florida’s billing regulations change frequently. Between new legislation, AHCA rule updates, and shifting federal requirements, staying compliant requires active monitoring and structured internal processes. Reactive compliance is how providers end up facing fines and audits.

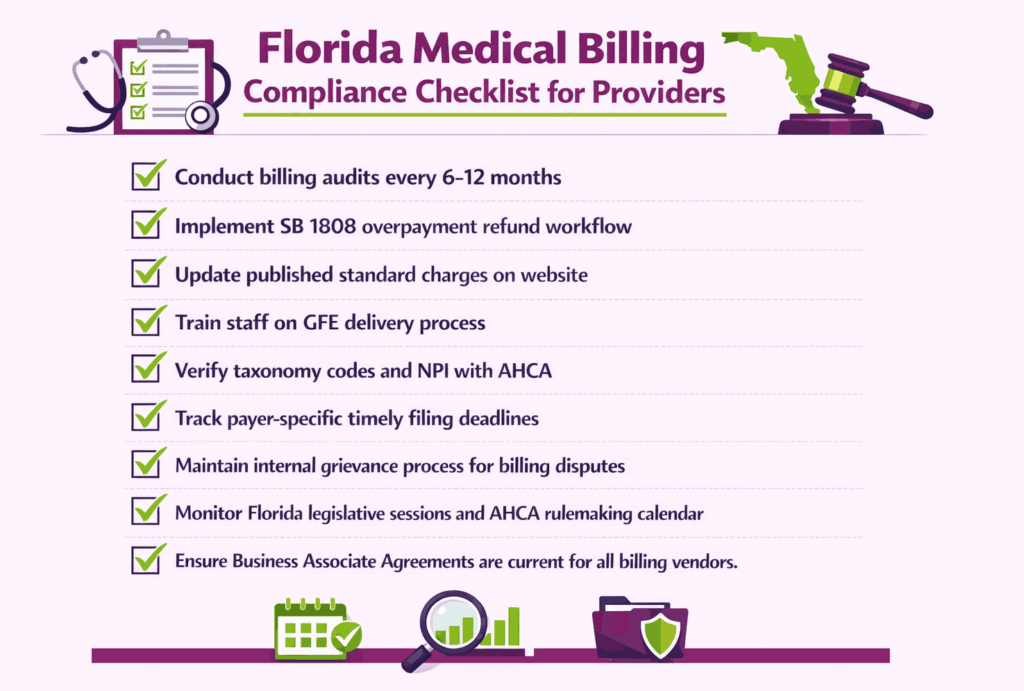

What Internal Processes Should Providers Establish for Billing Compliance?

Start with a billing audit cycle. Providers should conduct internal audits at least every six to twelve months, reviewing claim accuracy, denial patterns, timely filing performance, and overpayment detection. SB 1808 makes overpayment audits non-negotiable. If your billing team cannot identify overpayments within the 30-day refund window, you are already out of compliance.

Price transparency workflows need to be in place as well. Licensed facilities must keep their published standard charges current on their website. Good Faith Estimates must be delivered to uninsured and self-pay patients within the required timeframe. Staff handling patient intake should be trained on when and how to generate these estimates.

Billing dispute handling is another area that needs a defined process. Florida law requires facilities to have an internal grievance process for patients to challenge charges. The patient liaison’s phone number must appear on every itemized statement. If a patient requests billing records for verification, the facility must deliver them within 10 business days.

What Role Does the Agency for Health Care Administration (AHCA) Play in Billing Oversight?

AHCA is the primary state-level regulator for healthcare facility licensing, Medicaid program administration, and billing compliance enforcement. It conducts inspections, processes complaints through the Florida Health Care Complaint Portal, and audits Medicaid claims through the Office of Medicaid Program Integrity.

AHCA also drives rulemaking under Chapter 59G of the Florida Administrative Code. These rules govern reimbursement schedules, billing codes, coverage policies, and managed care plan contracts. When AHCA updates a rule, providers are expected to adjust their billing operations accordingly. Ignorance of a rule change is not a defense against a compliance violation.

For facilities, AHCA has the authority to impose administrative fines, require corrective action plans, and, in severe cases, suspend or revoke licenses. For Medicaid-specific violations, AHCA can recoup overpayments directly and refer fraud cases for federal prosecution.

What Should Providers Do When a Florida Billing Law Changes?

Track legislative sessions. Florida’s legislative session typically runs from March through May each year. Bills signed into law can take effect immediately, on July 1, on October 1, or on January 1 of the following year. Providers need to know not just what passed but when each law becomes enforceable.

Monitor AHCA’s rulemaking calendar for updates to Chapter 59G. These rule changes can affect fee schedules, billing codes, and compliance requirements without any new legislation being passed.

When a new law or rule takes effect, update billing workflows before the effective date. Train staff on the specific changes and document the training. If the change is complex, such as SB 1808‘s refund requirements or SMMC 3.0‘s performance metrics, engage legal counsel or your RCM partner for an impact analysis before the deadline hits.

Frequently Asked Questions About Florida Medical Billing Laws

What is the Florida Medical Billing Statute of Limitations?

The general statute of limitations for medical debt in Florida is five years under Section 95.11(2)(b). This applies to most providers billing under written contracts. However, licensed facilities like hospitals and ambulatory surgical centers now face a shorter three-year window for filing debt collection lawsuits under the Live Healthy Act (HB 7089), effective October 1, 2024. After these deadlines pass, the debt becomes time-barred and cannot be pursued through the courts.

Is Balance Billing Illegal in Florida?

Balance billing is prohibited in specific situations. For emergency services, out-of-network providers cannot balance bill patients enrolled in Florida-licensed HMO, PPO, or EPO plans. For non-emergency services at in-network facilities, out-of-network providers in certain specialties are also barred from balance billing. HMO members have the broadest protection — Florida law prohibits all balance billing of HMO members by out-of-network providers, including in non-emergency settings. Outside of these protected scenarios, balance billing may be permitted depending on the plan type and whether the patient gave written consent.

How Long Does a Provider Have to Refund a Patient Overpayment in Florida?

Thirty days from the date the provider determines an overpayment occurred. This requirement comes from SB 1808, effective January 1, 2026. It applies to licensed facilities and practitioners who have billed a government program, private insurer, or HMO. Facilities face fines up to $500 per day for each violation. Practitioners face disciplinary action, including potential license suspension.

What Happens if a Florida Provider Violates Medical Billing Laws?

Penalties depend on the violation. AHCA can fine licensed facilities up to $500 per violation per day for billing infractions. The Florida Department of Health can take disciplinary action against individual practitioners, ranging from fines to license revocation. For Medicaid billing fraud, AHCA’s Office of Medicaid Program Integrity can recoup payments and refer cases to the Department of Justice. HIPAA violations add a separate layer of federal penalties starting at $145 per violation and reaching over $2 million for willful neglect. In all cases, the provider may also face state-level enforcement from the Florida Attorney General.

Can a Hospital Sue You for Medical Debt in Florida?

Yes, but within limits. Licensed facilities must follow the extraordinary collection action rules under Section 395.3011 before pursuing legal action. They must first make reasonable efforts to determine if the patient qualifies for charity care and provide advance written notice before initiating a lawsuit, selling the debt, or reporting it to credit agencies. The lawsuit must also be filed within the three-year statute of limitations established by the Live Healthy Act.

What is the No Surprises Act, and How Does It Apply in Florida?

The No Surprises Act is a federal law effective January 2022 that protects patients from unexpected out-of-network bills for emergency services and certain non-emergency services at in-network facilities. It also requires providers to give uninsured patients a Good Faith Estimate before scheduled services. In Florida, the NSA works alongside state balance billing laws. Where Florida law provides stronger protections, such as the blanket ban on balance billing for HMO members in non-emergency settings, state law takes precedence.