New Jersey operates one of the most regulated healthcare billing environments in the country. State law frequently goes further than federal minimums, and practices that miss the distinction pay for it in denied claims, fines, or voided debt.

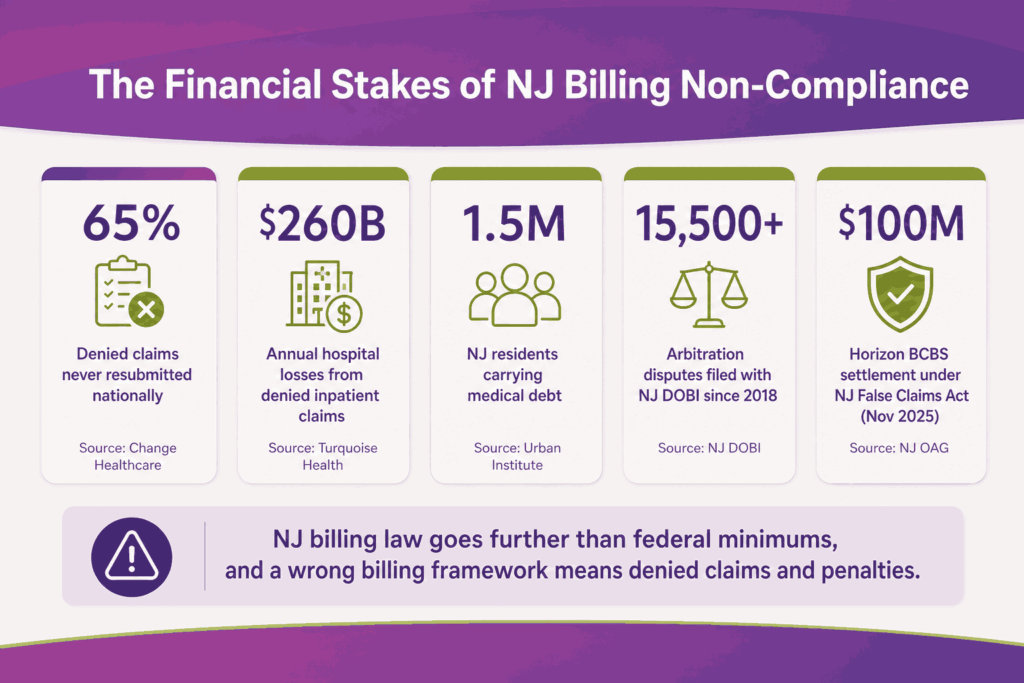

Nationally, 65% of denied claims are never resubmitted, and hospitals lose $260 billion in denied inpatient claims annually. In the high-compliance environment of New Jersey, with over 15,500 arbitration disputes filed with the DOBI since 2018, the financial impact is even greater. Without structured follow-up, denied claims quickly turn into permanent write-offs.

This guide covers every active NJ billing law affecting medical billing providers in New Jersey in 2026, including what changed, who it applies to, the penalty exposure, and what your billing team must do now.

Why New Jersey Billing Compliance Is More Complex Than Most States

New Jersey billing compliance is more complex than most states because providers must operate under two overlapping systems. State laws apply to fully insured plans, while federal rules govern self-funded ERISA plans, which make up the majority of the commercial market. Each framework follows different rules for reimbursements, appeals, and dispute resolution. Using the wrong pathway can delay payments or lead to failed claims.

The regulatory burden is also heavier than average. Since the state’s 2018 surprise billing law, providers must meet strict disclosure, documentation, and arbitration requirements on out-of-network care. These rules continue to expand with newer legislation focused on prior authorization and billing transparency, adding more checkpoints across the revenue cycle.

At the time recent reforms were introduced, about 1.5 million New Jersey residents carried medical debt, highlighting the state’s focus on tighter billing and patient protection. In parallel, enforcement actions have led to multi-million-dollar settlements. In November 2025, Horizon Blue Cross Blue Shield paid $100 million under the NJ False Claims Act, which was the state’s largest-ever non-Medicaid billing fraud settlement.

With dense payer variation and continuous regulatory updates, even small errors can quickly result in denials, audits, or delayed revenue. The nine active NJ billing laws this article covers are:

- The Out-of-Network Consumer Protection, Transparency, Cost Containment, and Accountability Act

- The Louisa Carman Medical Debt Relief Act

- The Ensuring Transparency in Prior Authorization Act / ETPAA

- The NJ Pharmacy Benefit Manager Oversight Act

- The NJ Hospital Care Payment Assistance Program / Charity Care requirements

- NJ Itemized Billing and Medical Records Laws

- The NJ False Claims Act and NJ Insurance Fraud Prevention Act

- The ACF Gross Receipts Assessment Cap

- The NJ Menopause Coverage Act

Law 1: NJ Out-of-Network Consumer Protection and Surprise Bill Act

Governor Murphy signed this law on June 1, 2018. It went into effect on August 30, 2018. The full name is the Out-of-Network Consumer Protection, Transparency, Cost Containment, and Accountability Act.

It applies to NJ health care facilities, individual providers, insurance carriers, and self-funded plans that have opted in. Medicare, NJ FamilyCare/Medicaid, and TRICARE are not covered by this law.

Core Provisions

- Balance billing prohibition: Providers cannot bill patients beyond in-network cost-sharing amounts for emergency, urgent, or inadvertent out-of-network services. If a patient is treated at an in-network hospital by an OON anesthesiologist, that provider cannot bill the patient for the difference.

- Pre-service disclosure requirement: Facilities and providers must disclose network status, medical codes, and estimated fees before scheduling any non-emergency procedure.

- Mandatory assignment of benefits: For inadvertent OON or emergency services, benefits automatically transfer to the OON provider with no action required from the patient.

- Prohibition on cost-sharing waivers: OON providers cannot waive patient deductibles or copays to attract patients. Federal safe harbors are exempt.

Arbitration Process

When a payer and provider cannot agree on payment and the disputed amount exceeds $1,000, either party can trigger binding arbitration. The process follows a baseball-style format, where an arbitrator selects one of two submitted final offers.

| Arbitration Step | Responsible Party | Timeline |

|---|---|---|

| Pay or flag bill as excessive | Insurance carrier | Within 20 days of receiving the claim |

| Dispute and negotiate payment | Provider | Within 30 days of carrier’s response |

| Select one final submitted offer | Arbitrator | Within 30 days of arbitration filing |

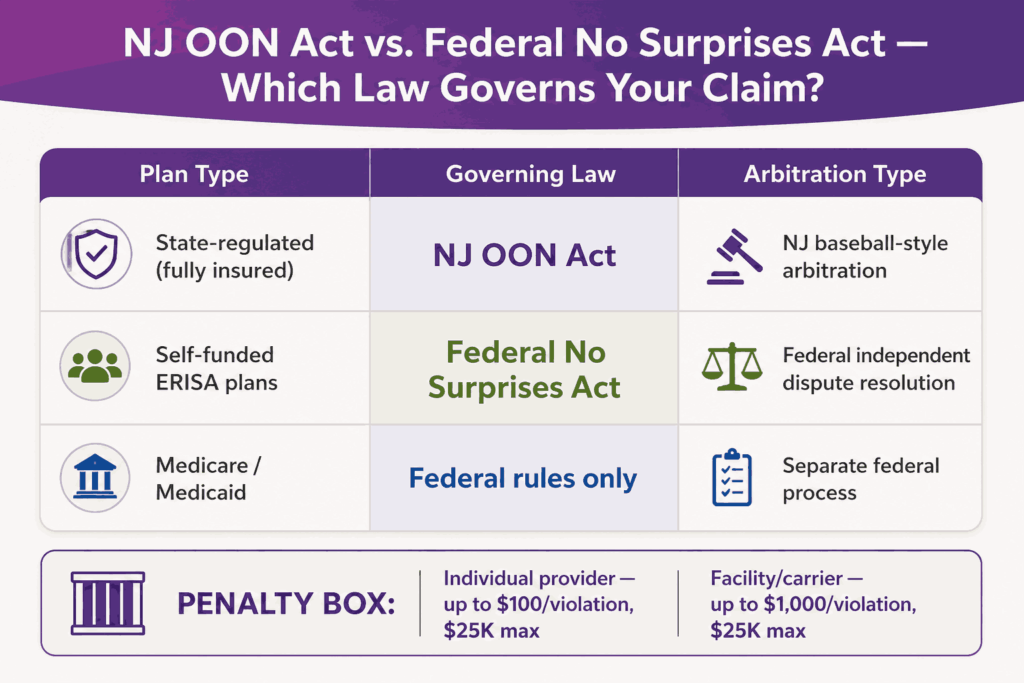

Difference Between NJ Act vs. Federal No Surprises Act

| Plan Type | Governing Law | Arbitration Process |

|---|---|---|

| State-regulated (fully insured) | NJ OON Act | NJ baseball-style arbitration |

| Self-funded ERISA plans | Federal No Surprises Act | Federal independent dispute resolution |

| Medicare / Medicaid | Federal rules only | Separate federal process |

Self-funded ERISA plans represent the majority of commercially insured NJ patients. Submitting a claim under the wrong arbitration process wastes time and may waive provider rights.

Penalties for Non-Compliance

| Violating Party | Fine Per Violation | Maximum Cap |

|---|---|---|

| Individual health professional | Up to $100 | $25,000 per occurrence |

| Hospital, clinic, or carrier | Up to $1,000 | $25,000 per occurrence |

The NJ Department of Banking and Insurance (DOBI) handles enforcement. Non-compliant physicians can be referred to their licensing board.

How to Ensure Compliance For Your Practice

- Build OON identification into your pre-claim scrubbing workflow

- Document pre-service disclosure for every scheduled procedure

- Create a consent protocol for patients who voluntarily choose an OON provider

- Set up an arbitration tracking workflow for any disputed claim over $1,000

Law 2: Louisa Carman Medical Debt Relief Act

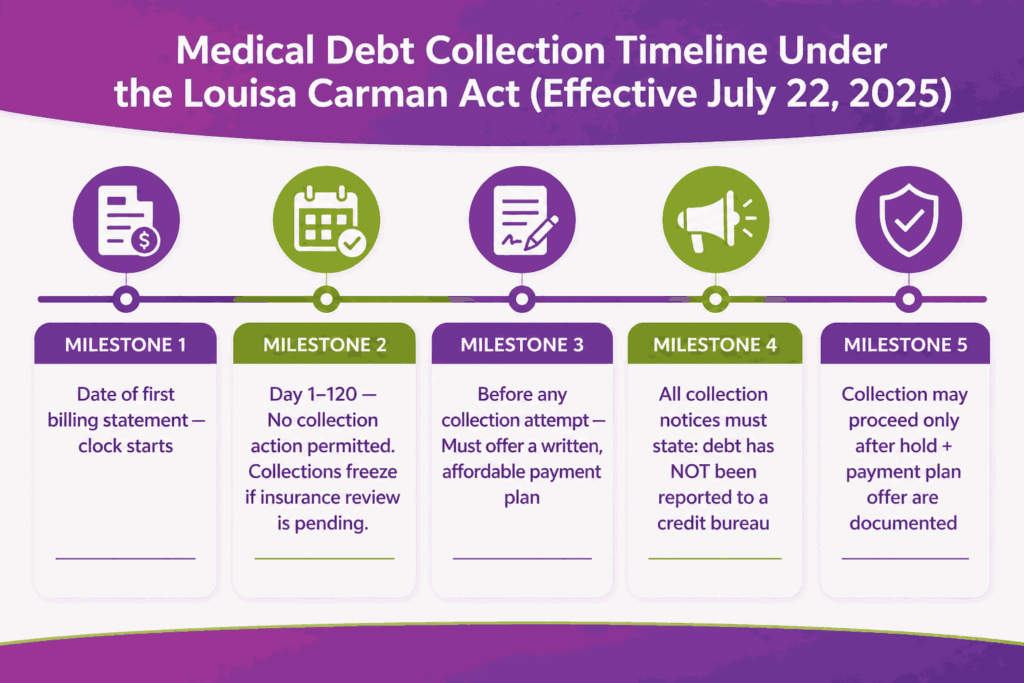

Governor Murphy signed Assembly Bill 3861 on July 22, 2024. The credit reporting ban took effect immediately. All remaining provisions activated on July 22, 2025, and are now in full effect. The law is named after Louisa Carman, a Murphy administration staffer who was the law’s chief architect before her death in January 2024.

What the Law Requires from Providers

Credit reporting ban: Providers and debt collectors cannot report medical debt to consumer reporting agencies for services rendered on or after July 22, 2024. Any violation makes that debt void and exposes the provider to civil liability under the NJ Fair Credit Reporting Act.

Exceptions to the credit reporting ban include:

- Debt backed by collateral

- Debt owed to veterinarians

- Certain loan-based medical debt

- Debt on credit cards issued solely for healthcare costs

- Insurance payments the patient received and kept

Required collection notice: Any collection attempt must include a written notice stating that the debt has not been reported to a consumer reporting agency.

120-day pre-collection hold: Providers must wait 120 days after the first billing statement before beginning any collection action, regardless of patient communication.

Mandatory payment plan requirement: Before pursuing collection, providers must offer a reasonable payment plan with monthly amounts the patient can afford.

Collection freeze during insurance review: Providers cannot send collection communications or file lawsuits while an internal or external insurance review of a claim is pending.

Financial Protection Provisions

| Provision | Details |

|---|---|

| Interest rate cap | Maximum 3% per annum on medical debt, including court judgments |

| Wage garnishment ban | Prohibited for patients earning below 600% federal poverty level |

| 2024 income threshold | ~$90,360 individual; ~$187,200 for a family of four |

| Ongoing collection freeze | No action while patient is complying with a payment plan |

Federal Preemption Challenge

The federal CFPB rule that would have banned medical debt from credit reports nationwide was vacated by the U.S. District Court for the Eastern District of Texas on July 11, 2025, after the CFPB under the Trump administration agreed with plaintiffs that the rule exceeded its statutory authority.

Beyond killing the federal rule, the Texas court went further. It stated that the Fair Credit Reporting Act (FCRA) preempts state laws that attempt to impose similar restrictions on credit reporting. Legal experts note this language is dicta, meaning it was not the direct issue before the court and carries no binding precedent. However, debt collection industry groups have already filed lawsuits using this argument to challenge state-level medical debt credit reporting bans, starting with Colorado.

What this means for NJ providers:

- NJ’s credit reporting ban remains in full legal effect as of April 2026. No court has struck it down.

- A successful preemption challenge in another state could create risk for NJ’s ban. Monitor DOBI guidance and any NJ-specific litigation closely.

- Your medical debt collections vendor contracts should include indemnification language in the event of a preemption ruling.

- Do not relax credit bureau reporting controls based on speculation. Operate as if the NJ ban is fully enforceable because it currently is.

Revenue Cycle Impact

The 120-day hold reshapes AR aging for any practice with high patient-pay volume. Payment plan processes that were previously informal are now legally required steps before escalation. Collections vendors operating on behalf of NJ providers must also comply, which means vendor contracts need to reflect these requirements.

How to Ensure Compliance

- Build the 120-day pre-collection hold into AR aging buckets

- Create a documented payment plan offer process with a record of patient response

- Add the required disclosure notice to all collection communications

- Disable credit bureau reporting for covered NJ medical debt

- Add income screening before initiating wage garnishment

- Monitor federal preemption litigation involving state medical debt credit reporting laws

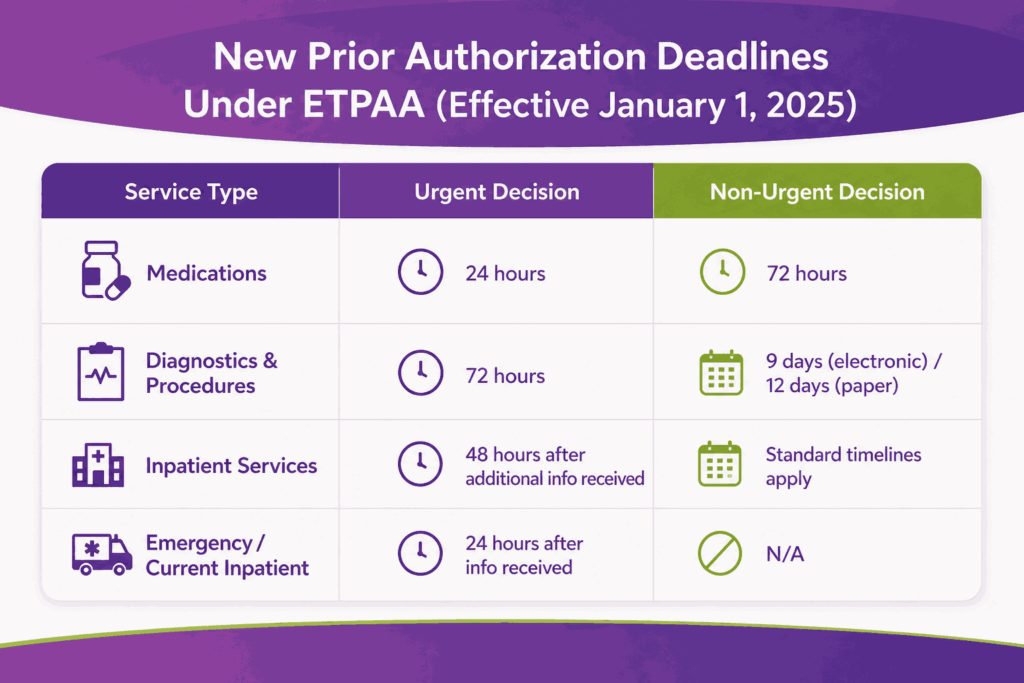

Law 3: Ensuring Transparency in Prior Authorization Act (ETPAA)

Governor Murphy signed AB 1255 / SB 1794 in January 2024. The Ensuring Transparency in Prior Authorization Act (ETPAA) replaced the Health Claims Authorization, Processing and Payment Act (HCAPPA) and took effect January 1, 2025.

The law applies to state-regulated health plans, the State Health Benefits Program, and the School Employees’ Health Benefits Program. It does not apply to NJ FamilyCare, Medicaid, or self-funded ERISA plans.

New Decision Timelines

| Service Type | Urgent PA Deadline | Non-Urgent PA Deadline |

|---|---|---|

| Medications | 24 hours | 72 hours |

| Diagnostics and procedures | 72 hours | 9 days (electronic) / 12 days (paper) |

| Inpatient services | 48 hours after additional information received | Standard timelines apply |

| Emergency or current inpatient | 24 hours after information received | N/A |

Specialty-Reviewer Requirement

If a prior authorization request is denied, the review must be conducted by a physician of the same specialty as the treating physician. This rule closes a major gap that previously allowed non-specialist reviewers to deny specialty care requests.

For pain management, psychiatry, and oncology practices, this provision gives a strong legal basis for appealing mismatched denials.

Continuity of Care Protections

- Plan switching coverage: When a patient switches health plans, the new carrier must honor prior authorizations from the old plan for 60 days. This protects billing continuity for ongoing treatment protocols.

- Chronic condition PA validity: Prior authorizations for chronic or long-term conditions remain valid for 180 days, reducing repeated PA submissions for the same patient.

- Mandatory public reporting: Carriers must publish prior authorization denial data on their websites, giving billing teams a tool to benchmark denial rates by payer and service type.

How To Ensure Compliance

- Update PA tracking systems with the new decision timelines per service category.

- Build 72-hour and 24-hour escalation triggers into your PA workflow

- Train staff on the specialty-reviewer denial appeal right and how to document it

- Log chronic condition PAs with 180-day validity dates to avoid unnecessary resubmissions

Law 4: NJ Pharmacy Benefit Manager Oversight Act

Assembly Bill 536 established state-level licensing requirements for Pharmacy Benefit Managers (PBMs) operating in New Jersey. Any business entity acting as a PBM without DOBI licensure is in direct violation of state law. Pharmacy Service Administrative Organizations (PSAOs) must also register separately.

The law also establishes new transparency standards, data reporting requirements, and restrictions on how PBMs set drug costs.

Impact on Specialty Billing

This law most directly affects practices billing for specialty drugs or in-office medications. Pain management, oncology, and psychiatry practices that rely on PBMs for specialty drug prior authorizations are now part of a stricter accountability chain.

If a PBM involved in your billing workflow is not licensed with NJ DOBI, the validity of their PA decisions and the accuracy of their remittances can be challenged. That creates downstream risk on claims you may have already processed.

What Compliance Action Steps You Can Take

- Verify that all PBMs your practice works with hold a current NJ DOBI license

- If your practice dispenses medications, confirm PSAO registration status

- Update pharmacy billing workflows to document licensed PBM status per claim type

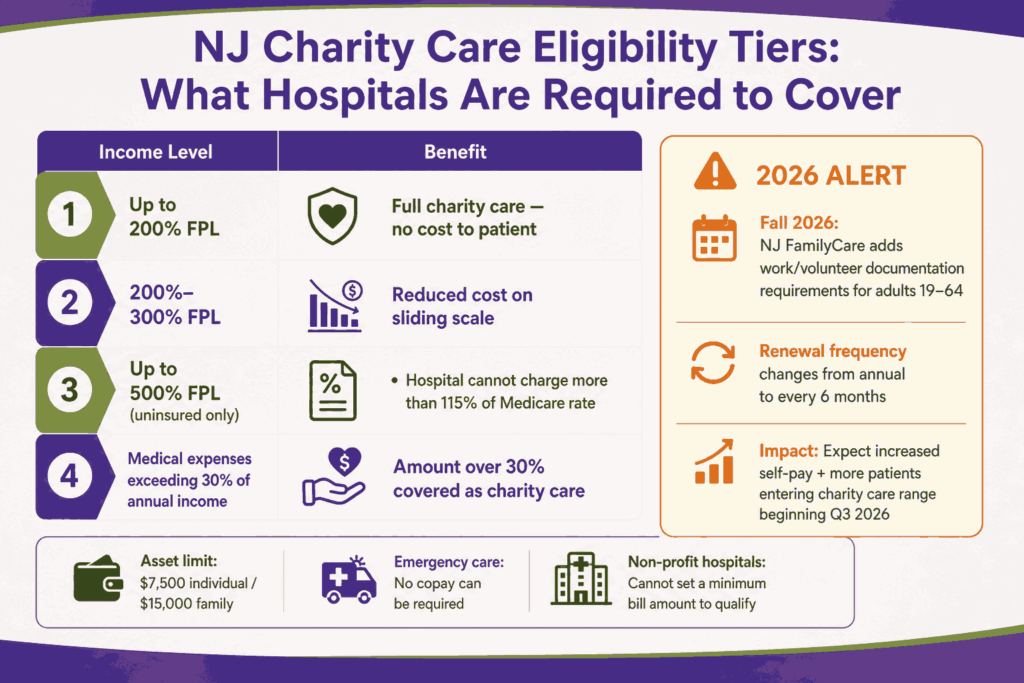

Law 5: NJ Hospital Care Payment Assistance Program (Charity Care)

All acute care hospitals in New Jersey are required by state law to provide charity care to patients who cannot afford to pay. This is not discretionary. Hospitals must provide free or reduced-cost care for all inpatient and outpatient services, regardless of a patient’s ability to pay.

| Income Level (as % of Federal Poverty Level) | Charity Care Benefit |

|---|---|

| Up to 200% FPL | Full charity care coverage at no cost |

| 200% to 300% FPL | Reduced cost on a sliding scale |

| Up to 500% FPL (uninsured) | Hospital may not charge more than 115% of the Medicare rate |

| Medical expenses exceeding 30% of annual income | Amount over 30% is covered as charity care |

The asset limit for charity care eligibility is $7,500 for an individual and $15,000 for a family. Hospital assistance is available to both NJ residents and non-residents in specific circumstances.

Screening and Billing Requirements

Hospitals must screen every patient for charity care eligibility before sending any bill to collections. Patients must also be informed about NJ FamilyCare and Medicaid options within three months of the date of service.

Providers cannot send charity-care-eligible patients to collections without first completing the eligibility determination process. Emergency care copays cannot be required. Non-profit hospitals cannot require a minimum bill amount for a patient to qualify.

2026 Update: Federal Medicaid Funding and FamilyCare Eligibility Changes

Two federal-level changes now affect charity care volume and funding for NJ hospitals. The details of both of them are as follows:

- NJ FamilyCare Eligibility Contract (Fall 2026) – The federal “One Big Beautiful Bill Act,” signed by President Trump in July 2025, introduces community engagement requirements for NJ FamilyCare members. Starting Fall 2026, certain adults aged 19 to 64 must document work, volunteer hours, or educational enrollment to maintain coverage. These members must also renew every six months instead of every twelve.

- Medicaid Funding Environment – In December 2025, the NJ Department of Health announced federal approval of approximately $540 million in Medicaid outpatient state-directed payment funding for SFY2026. Proper charity care documentation is a prerequisite for accessing that funding. However, federal Medicaid funding levels for SFY2027 and beyond are under active pressure from federal budget legislation. Hospitals should not treat the $540M figure as a stable forward baseline.

How To Ensure Compliance

- Build a charity care eligibility screening step into your admission and billing workflow

- Provide written notices about charity care and Medicaid options within three months of service

- Block collections escalation until charity care eligibility is confirmed

- Maintain documentation of applications and determination outcomes

- Begin modeling self-pay volume increases ahead of Fall 2026 FamilyCare eligibility changes

Law 6: NJ Itemized Billing and Medical Records Requirements

This NJ law requires providers to deliver a consolidated, itemized billing statement to patients. The delivery timelines are:

- Within 30 days of discharge or release

- Within 7 days of a written patient request

Billing statements must be written in plain language that any ordinary person can understand. Technical terms are permitted only if defined within the document.

What an Itemized Statement Must Include

- Each service listed by date and provider

- Unit pricing at the department level

- Drug entries using brand or generic name, not drug codes alone

- Services from hospital-based physicians who cannot separately bill

- Payment status of each line item (paid, payer-assigned, or patient-responsible)

Each facility must also have a written process to respond to patient billing questions within 7 business days of receiving the inquiry.

Medical Records Requirements (NJ.S.A. 26:2H-5n and 45:9-22.27)

- Providers cannot withhold records due to an unpaid balance if the records are needed for continuing care

- No charge for records when a provider terminates a patient or leaves a practice

- Records that are illegible or not in English must be translated at no cost to the patient

- Records must be delivered in the format and to the address the requester specifies

Third-Party Billing Service Certification

Since January 1, 2002, any entity acting as a third-party billing service in NJ must hold state certification from the DOBI Commissioner. This applies to any organization that submits claims or accepts payer remittances on behalf of providers. Operating without certification is a direct violation of state law.

Providers who outsource medical billing must verify their partner’s NJ certification before any contract is signed.

How To Ensure Compliance

- Audit billing statements against itemized billing requirements; build 30-day / 7-day delivery timelines into workflows

- Create a written billing inquiry response process with a 7-business-day deadline

- Verify your billing partner holds a valid NJ DOBI third-party billing service certification

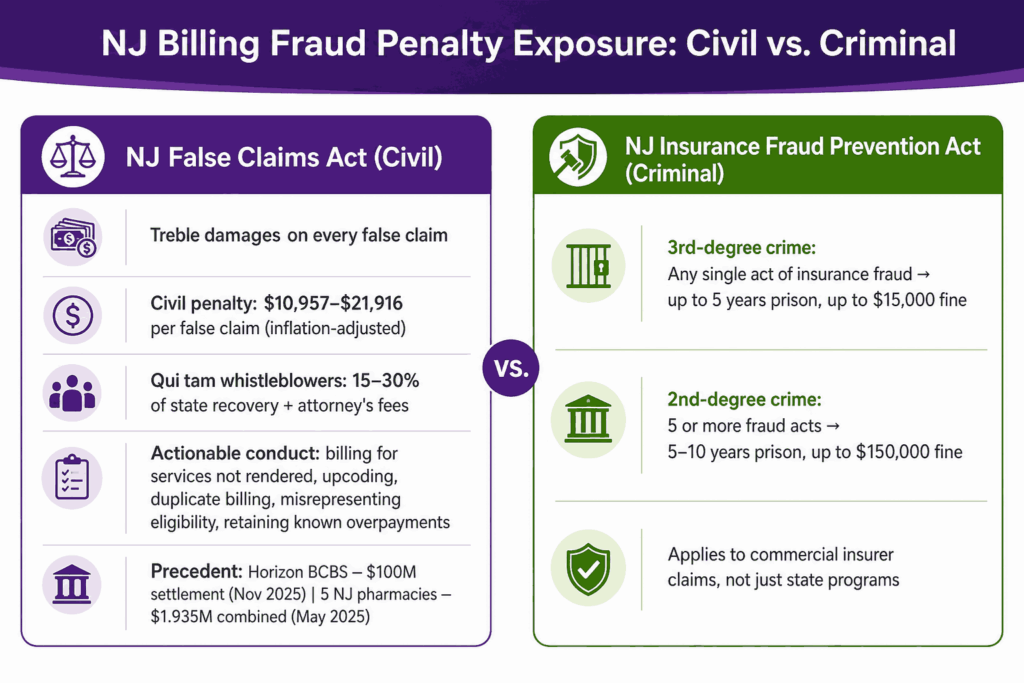

Law 7: NJ False Claims Act and Insurance Fraud Prevention Act

The NJ False Claims Act (NJFCA) was enacted in 2008 and amended in June 2023 to align more closely with the federal False Claims Act. The 2023 amendment also made NJ eligible for a 10 percent enhancement in Medicaid fraud recoveries from the federal government.

The NJFCA allows the NJ Attorney General and private whistleblowers to bring civil lawsuits against providers that submit false claims to the state or its programs.

Actionable conduct in a billing compliance context includes:

- Billing for services not rendered

- Upcoding (billing a more expensive procedure than what was performed)

- Duplicate billing

- Misrepresenting patient eligibility

- Retaining known overpayments

Penalties: Treble damages plus civil penalties currently between $10,957 and $21,916 per false claim, adjusted for inflation.

Qui tam provisions: Whistleblowers can file lawsuits on the state’s behalf and collect a bounty of 15 to 30 percent of the state’s recovery, plus attorneys’ fees. This creates significant internal compliance risk.

Enforcement precedent: In November 2025, Horizon Blue Cross Blue Shield agreed to pay $100 million under the NJFCA for systematically overcharging the state. In May 2025, five NJ pharmacies paid a combined $1.935 million for billing Medicare Part D and NJ Medicaid for medications never dispensed.

NJ Insurance Fraud Prevention Act

Separate from the NJFCA, the NJ Insurance Fraud Prevention Act makes it a criminal offense to submit misleading information in connection with an insurance claim. This includes billing claims submitted to commercial insurers.

| Offense Level | Conduct | Penalty |

|---|---|---|

| Third-degree crime | Any single act of insurance fraud | Up to 5 years in prison, up to $15,000 fine |

| Second-degree crime | Five or more insurance fraud acts | 5 to 10 years in prison, up to $150,000 fine |

What Compliance Action Steps Can Be Taken

- Conduct regular internal coding audits against the services documented

- Establish a written process for identifying and refunding known overpayments promptly

- Build a whistleblower protection and internal reporting policy for billing staff

- Do not submit claims for services where documentation does not support the code billed

Law 8: ACF Gross Receipts Assessment Cap

Governor Murphy signed Senate Bill 5015 on January 20, 2026, one of his final acts before leaving office. The law imposes an annual cap of $2 million per ambulatory care facility (ACF) on the uniform gross receipts assessment. The cap took effect on January 1, 2026.

Prior to this law, ambulatory surgery centers and other ACFs faced uncapped gross receipts assessments that scaled with revenue. For high-volume facilities, this created significant and unpredictable tax exposure.

Who It Affects

- Ambulatory surgery centers (ASCs)

- Outpatient surgical facilities

- Endoscopy centers

- Other facility types classified as ACFs under NJ law

How Does It Impact Revenue Cycle

The $2 million cap creates a fixed ceiling on assessment liability for higher-revenue ACFs. This is a direct financial benefit that should be reflected in SFY2026 budget projections. Billing and finance teams at ACF-class facilities should confirm their facility’s assessment baseline and verify the cap applies to their specific license type.

Compliance Action Steps

- Confirm your facility is classified as an ACF under NJ law

- Update SFY2026 financial projections to reflect the $2 million assessment cap

- Verify with your finance team whether the cap changes net revenue calculations

Law 9: NJ Menopause Coverage Act

Governor Murphy signed the NJ Menopause Coverage Act on January 9, 2026. The law requires health insurance coverage for medically necessary treatments for perimenopause and menopause across a wide range of plan types.

Covered Services

- Hormonal and non-hormonal therapies

- Behavioral health care related to menopause

- Pelvic floor physical therapy

- Bone health screenings and medications

- Counseling and education regarding treatment options

Billing Implications

This law expands covered service codes for OBGYN billing, primary care billing, and behavioral health practices treating perimenopausal or menopausal patients. Any practice currently treating patients for menopause-related conditions should audit their payer contracts to confirm coverage alignment with the new state mandate.

Practices in psychiatry and behavioral health should note that behavioral health care for menopause is explicitly covered, which may create new authorization and coding pathways that did not previously exist for this patient population.

Plan Types Covered

Coverage applies to state-regulated health plans. Providers should verify applicability for self-funded ERISA plans, as federal law governs those separately. Contact individual payers to confirm how they are implementing the mandate for plans renewing in 2026.

How To Ensure Compliance

- Audit current coding for menopause-related services against new covered service categories

- Verify payer contracts reflect the new coverage mandate for OBGYN and behavioral health services.

- Update PA workflows for newly covered service types that may require prior authorization.

Hospital Price Transparency: Federal Requirements with NJ Enforcement Implications

Since January 1, 2021, CMS has required all hospitals to publicly post standard charges for all items and services. In May 2025, CMS issued updated guidance requiring hospitals to disclose actual prices, not estimates. Hospitals should expect increased CMS audit activity for non-compliance.

Fewer than 50 percent of NJ hospitals are currently fully compliant with federal price transparency requirements, according to data cited in the NJ State Legislature during debates on pending legislation.

NJ-Level Enforcement Risk: A5376 Status Update

Assembly Bill A5376 would create a Health Care Cost Containment and Price Transparency Commission, establish a state Office of Healthcare Affordability and Transparency, and prohibit non-transparent hospitals from collecting medical debt from patients treated during a non-compliant period. A civil penalty of $10 per day per hospital bed would also apply.

2026 Update: As of April 2026, A5376 remains stalled. The bill passed out of the Assembly Financial Institutions and Insurance Committee in June 2025 with amendments and was referred to the Assembly Appropriations Committee, where it has not advanced. Advocates have publicly called for action, but no floor vote has been scheduled. This bill is not law. CMS enforcement of the existing federal rule remains the primary compliance risk.

What Compliance Action Steps Should Be Taken?

- Verify your hospital’s machine-readable price file and shoppable services list are current and publicly posted.

- Confirm posted prices reflect actual charges, not estimates, per May 2025 CMS guidance.

- Assign someone to monitor CMS audit correspondence if your facility is behind on compliance.

- Track A5376 for committee movement in the 2026-2027 legislative session

NJ vs. Federal Billing Law: Quick Reference for Providers (Updated 2026)

| Legal Area | State-Regulated Plans | Self-Funded ERISA Plans | Medicare/Medicaid |

|---|---|---|---|

| Surprise billing / balance billing | NJ OON Act | Federal No Surprises Act | Federal rules |

| Prior authorization timelines | ETPAA | Not covered by ETPAA | CMS federal PA rules |

| Medical debt credit reporting | NJ ban in full effect (preemption litigation active — monitor) | Federal CFPB rule vacated July 2025; no federal protection | Separate rules |

| Charity care obligations | NJ Hospital Care Payment Assistance Program | N/A | Separate DSH/Medicaid rules |

| False claims liability | NJ False Claims Act (state programs) | Federal FCA (Medicare/Medicaid) | Both may apply |

| Price transparency | Federal CMS rule (all hospitals) | Federal CMS rule | Federal CMS rule |

| Menopause coverage | NJ Menopause Coverage Act (2026) | Not mandated by NJ law | Federal/CMS rules |

| ACF gross receipts assessment | $2M cap per facility (SFY2026) | N/A | N/A |

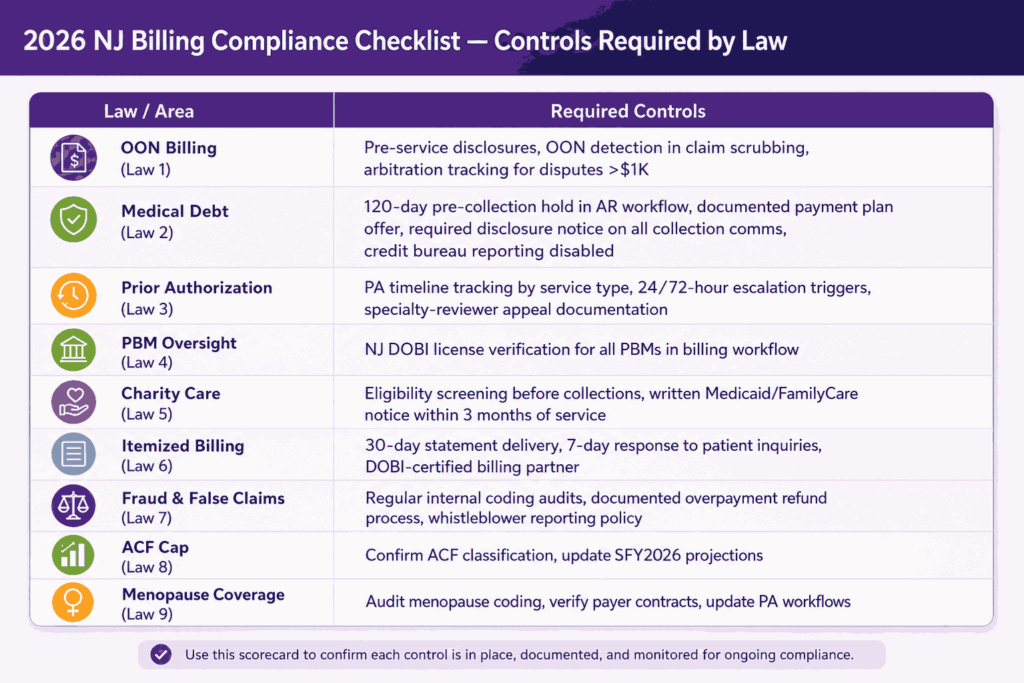

2026 NJ Billing Compliance Checklist

| Law / Area | What You Must Have in Place |

|---|---|

| Out-of-Network Billing | Pre-service disclosures, OON detection in scrubbing, arbitration workflows for disputes |

| Medical Debt Rules | 120-day hold before collections, documented payment plans, required disclosures |

| Prior Authorization | Timeline tracking, escalation triggers, appeal workflows |

| PBM Oversight | NJ DOBI licensing verification |

| Charity Care | Eligibility screening + delayed collections | Billing Transparency | Itemized statements + response timelines |

| Fraud & Compliance | Internal audits + overpayment refund process |

| New 2026 Updates | ACF cap adjustments + menopause coverage compliance |

With multiple laws overlapping, gaps often occur where processes are not clearly defined. This is especially true for practices without a certified NJ medical billing company managing compliance across the full revenue cycle. These gaps increase the risk of errors, delays, and lost revenue.

How a Compliant NJ Billing Partner Reduces Your Exposure

NJ billing law creates compliance overhead that grows with practice size and specialty complexity. A certified NJ third-party billing service is legally required to maintain state compliance standards.

When choosing from top medical billing companies in New Jersey, verify:

- Valid NJ DOBI third-party billing service certification

- OON claim identification in the pre-submission workflow

- PA tracking updated for ETPAA timelines

- Collections process built around the Louisa Carman Act requirements — including preemption monitoring

- Coding audit capabilities to reduce NJFCA exposure

- Familiarity with 2026 additions: ACF cap implications and Menopause Coverage Act coding

Transcure’s NJ billing team operates under current state law across the full revenue cycle. Schedule a compliance review to find where your current process has exposure.

Conclusion

Nine active NJ laws now govern provider billing at every stage, from scheduling through collections. The Louisa Carman Act provisions that were activated in July 2025 are the most urgent concern for any practice still using pre-2024 collections workflows. ETPAA prior authorization reform remains the next priority for specialty practices on manual PA tracking.

Two laws passed in January 2026 expand the compliance scope further. The ACF Gross Receipts Cap delivers a financial benefit for ambulatory surgery centers that should be reflected immediately in financial projections. The Menopause Coverage Act creates new covered service obligations for OBGYN, primary care, and behavioral health practices.

These updates make NJ billing compliance an ongoing process rather than a one-time fix. Outdated workflows increase the risk of delays, denials, and compliance gaps. Staying aligned requires continuous monitoring and updated billing controls.

Frequently Asked Questions

What Is The Louisa Carman Medical Debt Relief Act?

It is an NJ law signed in July 2024, with full provisions effective July 22, 2025. It bans medical debt credit reporting, requires a 120-day pre-collection hold, mandates payment plan offers, caps interest at 3% per year, and restricts wage garnishment for patients below 600% of the federal poverty level. As of 2026, the state ban remains enforceable despite federal preemption arguments being litigated in other states.

Are NJ Hospitals Required To Provide Free Care To Uninsured Patients?

Yes. All NJ acute care hospitals must provide charity care to patients whose income is at or below 200% of the federal poverty level. Patients between 200% and 300% FPL receive care at a reduced cost on a sliding scale. Beginning Fall 2026, NJ FamilyCare eligibility restrictions may increase the volume of patients entering the charity care range.

What Is The NJ False Claims Act, And How Does It Affect Providers?

The NJFCA allows the Attorney General and private whistleblowers to sue providers that submit false claims to state programs. Penalties include treble damages plus per-claim civil fines of $10,957 to $21,916. Amended in June 2023, it produced a $100 million enforcement settlement against Horizon Blue Cross Blue Shield in November 2025.

What Are The New 2026 NJ Billing Laws Providers Need To Know?

Two laws took effect in January 2026. Senate Bill 5015 caps the uniform gross receipts assessment for ambulatory care facilities at $2 million per ACF annually. The NJ Menopause Coverage Act requires health insurers to cover medically necessary menopause and perimenopause treatments, expanding covered service codes for OBGYN, primary care, and behavioral health billing.

What Does Federal Price Transparency Require From NJ Hospitals?

CMS requires all hospitals to publicly post standard charges. May 2025 guidance requires actual prices, not estimates. Non-compliant hospitals face CMS audits. Assembly Bill A5376, which would bar non-transparent hospitals from collecting patient debt, remains stalled in the Assembly Appropriations Committee as of April 2026.