Medical billing fraud is not a minor inconvenience. It is one of the most costly and persistent problems in the U.S. healthcare system. According to the National Health Care Anti-Fraud Association, healthcare fraud costs the United States between $100 billion and $170 billion every single year. This statistic shows just how widespread and financially damaging medical billing fraud truly is.

To help address this growing concern, this guide is designed to provide practical steps for identifying, responding to, and preventing medical billing fraud. By the end, you will know exactly how to identify a problem, build your evidence file, choose the right reporting channel, and understand the legal protections available to you.

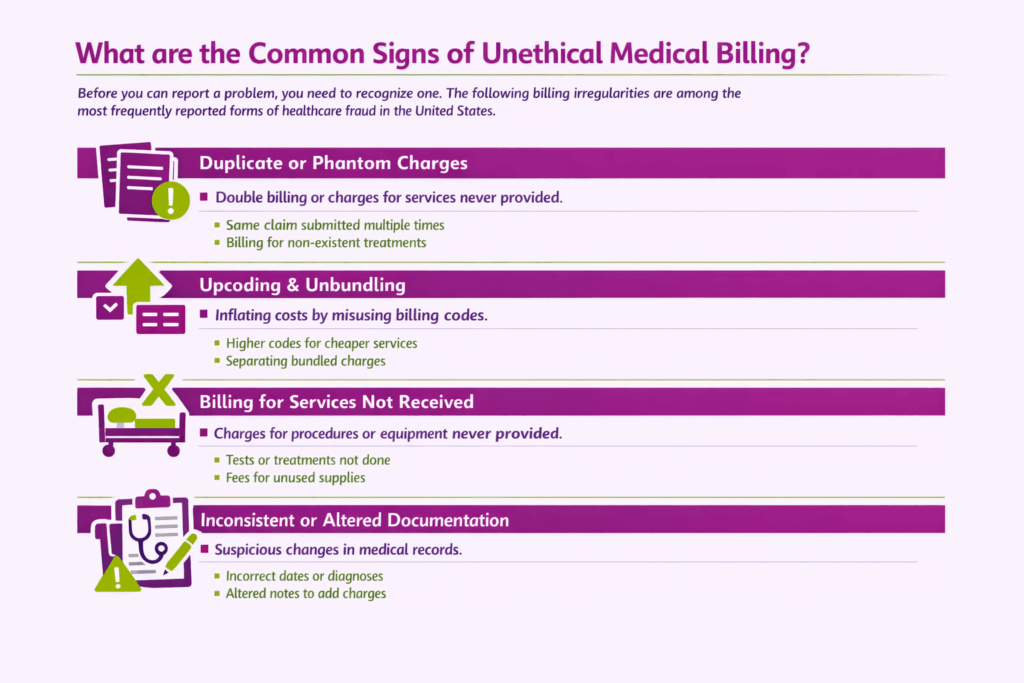

What are the Common Signs of Unethical Medical Billing?

Before you can report a problem, you need to recognize one. The following billing irregularities are among the most frequently reported forms of healthcare fraud in the United States.

Duplicate or Phantom Charges

Duplicate billing occurs when a provider submits the same claim more than once for a single service, either to the same insurer or to multiple payers simultaneously. Phantom billing takes this further by charging for services, procedures, or equipment that the patient never actually received. Both practices are forms of fraud and violate federal law.

Upcoding and Unbundling

Upcoding happens when a provider assigns a billing code for a more expensive service than the one actually performed. For example, a patient visits a clinic for a brief follow-up consultation, but the provider submits a code for a comprehensive new patient evaluation.

Unbundling is the practice of separating services that should be billed together under a single bundled code into multiple individual charges, which makes the final bill higher. Both upcoding and unbundling are among the most common forms of billing fraud investigated by the HHS Office of Inspector General.

Billing for Services Not Received

This category covers any scenario in which your medical bill includes charges for procedures, tests, medications, or medical equipment you did not receive. Examples include billing for an MRI that was ordered but never performed, or including fees for medical supplies that were never provided.

Inconsistent or Altered Documentation

Inconsistent or altered medical documentation is one of the more serious warning signs, as it may suggest deliberate fraud rather than accidental error. Red flags include treatment dates on your bill that do not match your appointment records and diagnosis codes that do not align with the reason for your visit. They may also include changes to medical records that appear to justify additional charges after the fact.

Where to Report Unethical Billing Practices?

The right reporting channel depends on the type of billing fraud involved, the payer affected, and the severity of the misconduct. Use the quick-reference table below, followed by detailed guidance for each channel.

| Agency / Body | Who to Contact | What They Handle |

|---|---|---|

| HHS OIG Hotline | 1-800-HHS-TIPS (oig.hhs.gov) | Medicare & Medicaid fraud |

| CMS No Surprises Help Desk | 1-800-985-3059 (cms.gov) | Surprise billing / out-of-network disputes |

| DOJ / False Claims Act | justice.gov/civil/false-claims-act | Large-scale fraud; qui tam whistleblower suits |

| FBI (ic3.gov) | ic3.gov | Systemic or organized healthcare fraud |

| State Attorney General | Find at naag.org | State-level billing fraud & consumer protection |

| State Medical Board | Find via FSMB.org | Provider license violations |

| Medicaid Fraud Control Unit | Find via oig.hhs.gov/fraud/medicaid-fraud-control-units | State Medicaid fraud |

| Your Insurance Company | Number on your insurance card | Private insurance billing errors & fraud |

Verifying the Issue Before Reporting

Not every billing discrepancy is fraud. Most of the time medical billing errors are the result of mistakes. Before escalating to a regulatory authority, you should consider resolving the issue directly.

Contacting the Provider or Billing Office

Your first call should be to the provider’s billing department. Use the phone number printed on your bill or the provider’s official website. When you call, have your bill, your Explanation of Benefits, and any relevant medical records in front of you.

Ask for an itemized bill if you have not already received one, hospitals and providers are legally required to provide one upon request. State clearly which charges you are disputing and why, and ask the representative to review those line items and provide a written explanation.

Keep a log of this conversation. You must note the date, time, the name of the person you spoke with, and a summary of what was said. This record will be valuable if you need to take action later.

Confirming If It’s a Mistake or Misconduct

Many billing errors resolve quickly at this stage. A transposed digit, wrong insurer, or incorrect bundling can often be fixed with a simple internal review. If the billing office acknowledges the error and corrects it promptly, document the resolution in writing.

However, if the provider insists the charges are correct, and you have documentation proving otherwise. Moreover, if the billing office is unresponsive, dismissive, or unable to explain the charges, that is a signal to escalate.

Documenting the Problem

Thorough documentation is the foundation of any successful billing complaint. Regulatory agencies can only act on evidence they can review, so the more organized and complete your documentation package is, the more effectively they can investigate.

Records and Evidence to Collect

Gather and retain the following materials before filing any complaint:

- All medical bills related to the dates of service in question, including original statements and any revised versions

- Itemized billing statements breaking down every individual charge

- Explanation of Benefits (EOB) from your insurance company corresponding to the same service dates

- Copies of your medical records for the relevant visits, including treatment notes, discharge summaries, and prescription records

- Any written correspondence with the provider or billing office, including letters, emails, and online portal messages

- A detailed log of all phone calls, including date, time, representative name, and summary of the conversation

- Your insurance card and policy documents showing coverage at the time of service

- Any good-faith estimate you received before the service, particularly for uninsured patients

Tips for Organizing Supporting Documentation

Disorganized documentation can slow an investigation or result in your complaint being dismissed for insufficient evidence. Follow these organizational principles:

- Create a dedicated folder, either physical or digital for the specific billing dispute. Label it clearly with the provider name, date of service, and the nature of the issue.

- Arrange documents in chronological order so investigators can follow the timeline of events easily.

- Make at least two copies of everything before submitting to any agency. One for your own records and one to submit.

- Use a simple tracking spreadsheet to list each document, its date, its source, and a one-line description of its relevance.

- Never submit originals to any agency unless specifically instructed to do so. Always retain your own copies.

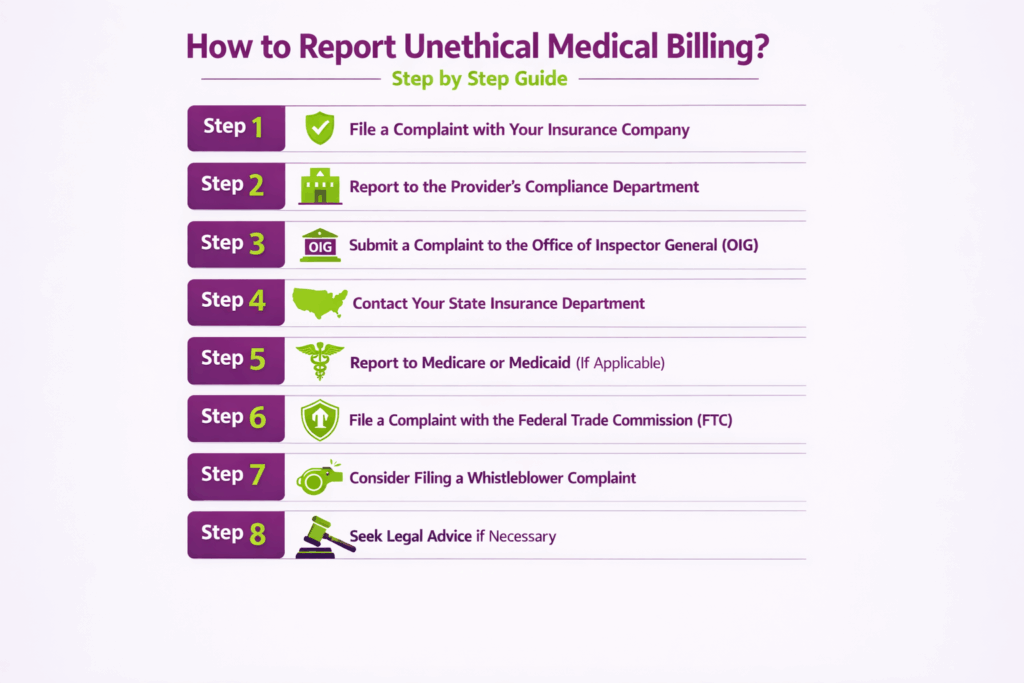

How to Report Unethical Medical Billing? Step-by-Step Guide

Once you have confirmed a problem and assembled your documentation, follow these steps in order.

Step 1: File a Complaint with Your Insurance Company

Start by contacting your health insurance provider. Use the customer service number on your insurance card or portal. Explain the issue clearly and provide supporting documents such as your bill and Explanation of Benefits (EOB). Insurers have fraud investigation units that can review suspicious claims and may resolve the issue directly with the provider.

Step 2: Report to the Provider’s Compliance Department

If the issue is not resolved, escalate it internally. Most hospitals and healthcare organizations have a compliance or ethics department. Submit a formal written complaint detailing the issue, along with your evidence. Many organizations also offer anonymous reporting options.

Step 3: Submit a Complaint to the Office of Inspector General (OIG)

For suspected fraud involving federal healthcare programs like Medicare or Medicaid, file a complaint with the U.S. Department of Health and Human Services Office of Inspector General. You can report online, by phone, or by mail. Provide as much detail and documentation as possible to support your claim.

Step 4: Contact Your State Insurance Department

Each state has a regulatory body that oversees insurance practices. File a complaint with your state’s insurance department if your insurer fails to address the issue or if the billing dispute involves policy violations.

Step 5: Report to Medicare or Medicaid (If Applicable)

If you are a beneficiary, you can report fraud directly to Medicare or Medicaid. They have dedicated fraud hotlines and online complaint systems to investigate improper billing practices.

Step 6: File a Complaint with the Federal Trade Commission (FTC)

For cases involving deceptive or unfair billing practices, you can report to the Federal Trade Commission. While the FTC does not resolve individual disputes, it uses complaints to identify patterns of fraud and take enforcement action.

Step 7: Consider Filing a Whistleblower Complaint

If you are a healthcare employee reporting fraud within your organization, you may qualify for protection under whistleblower laws such as the False Claims Act. This law allows individuals to report fraud against federal programs and may provide financial incentives if the case leads to recovery.

Step 8: Seek Legal Advice if Necessary

If the issue involves significant financial loss or ongoing fraud, consult a healthcare attorney. Legal professionals can guide you on filing formal claims, protecting your rights, and pursuing compensation if applicable.

What Happens After a Complaint Is Filed?

Filing a complaint is not the end of the process; it is the beginning. Understanding what to expect after you submit your report will help you stay informed and know when to follow up.

How Agencies Review Complaints?

Each agency has its own intake and review process. The HHS OIG, for example, reviews all complaints submitted to its hotline and determines whether they fall within its jurisdiction and whether there is sufficient evidence to warrant a formal investigation. Not every complaint will result in a full investigation.

Priority is given to cases involving larger dollar amounts, patterns of conduct across multiple patients, or fraud against federal programs. The CMS No Surprises Help Desk reviews surprise billing complaints to determine whether the No Surprises Act applies and whether the provider violated its rules. State medical boards review complaints to determine whether they implicate a licensed professional’s fitness to practice.

Possible Outcomes and Timelines

Timelines vary considerably depending on the complexity of the case and the volume of complaints an agency is managing. Simple billing errors resolved through direct provider contact may be corrected within days. Insurance fraud department investigations typically take weeks to months.

Federal investigations under the False Claims Act can take years, particularly if the government elects to intervene and build a prosecution. Possible outcomes range from administrative correction and refunds for individual patients to civil monetary penalties, provider exclusion from Medicare and Medicaid, and criminal prosecution in the most serious cases.

What Common Mistakes to Avoid When Reporting?

Even well-intentioned complainants can undermine their own case by making avoidable errors. Be aware of the following pitfalls before you submit your report.

Missing Documentation

The most common reason complaints are delayed is due to insufficient documentation. Agencies cannot investigate what they cannot verify. Before submitting any complaint, confirm that you have copies of all relevant bills, your EOB, and any communications with the provider.

Reporting Before Verification

Filing a formal complaint with a regulatory agency before first attempting to resolve the issue with the provider can slow the process unnecessarily. Follow the step-by-step escalation sequence outlined in this guide. Regulators generally expect to see evidence that you made an effort to resolve the matter directly before involving federal or state agencies.

Contacting the Wrong Agency

Routing your complaint to the wrong agency results in delays while your report is transferred or dismissed for lack of jurisdiction. Use the quick-reference table provided earlier in this guide to match your specific complaint to the correct authority.

Medicare and Medicaid fraud goes to the U.S. Department of Health and Human Services Office of Inspector General, while surprise billing violations go to the CMS No Surprises Help Desk.

State-licensed provider misconduct should be reported to the State Medical Board, and large-scale fraud against federal programs may warrant referral under the False Claims Act to the U.S. Department of Justice.

FAQs

How Do I Report Anonymously?

Yes, anonymous reporting is possible and accepted by several major agencies. The HHS OIG Hotline (1-800-HHS-TIPS) allows anonymous tips, as does the FBI’s Internet Crime Complaint Center at ic3.gov. Your state’s Attorney General and Medicaid Fraud Control Unit may also accept anonymous complaints. For qui tam cases under the False Claims Act, anonymity is not possible — your identity is filed with the court, though initially under seal.

What is a Qui Tam Lawsuit?

A qui tam lawsuit is a legal action brought by a private individual, known as a relator, under the False Claims Act on behalf of the government against organizations or entities committing fraud. These cases are commonly associated with fraud in sectors like healthcare, defense, or government contracting. If the case is successful, whistleblowers may receive 15% to 30% of the recovered funds as a reward for helping expose the fraud.

How can Healthcare Providers Prevent Medical Billing Fraud?

Healthcare providers can prevent medical billing fraud by implementing strict compliance measures, maintaining accurate documentation, and training staff on correct coding practices. Regular internal audits help identify errors or suspicious patterns early.

Outsourcing billing to reputable medical billing companies can also be highly effective. Professional services like Transcure specialize in accurate claim submission, up-to-date coding compliance, and thorough error checking, which helps minimize both accidental mistakes and potential fraud.

What Are the Legal Consequences of Engaging in Unethical Medical Billing Practices?

Engaging in unethical medical billing can lead to serious punishments under U.S. law, including both financial and criminal penalties:

- Repayment of Overbilled Amounts: Providers must refund any money received from insurers or patients for fraudulent or incorrect claims.

- Fines: Civil penalties under the False Claims Act range from $11,803 to $23,607 per false claim, plus treble damages (three times the loss to the government).

- Imprisonment: Criminal healthcare fraud convictions can result in up to 10 years in prison per offense.

- Exclusion from Federal Programs: Providers may be barred from Medicare and Medicaid.

- License Suspension or Revocation: State medical boards can suspend or revoke medical licenses for billing misconduct.

Why Should Practices Prioritize Ethical Medical Billing Services?

Choosing ethical medical billing services ensures your practice follows federal laws and avoids costly fraud investigations. These professional partners maintain honest coding standards to protect your reputation and financial health.

What are the Steps in a Medical Billing Complete Process?

The complete process of medical billing starts with patient registration and ends when the final payment is collected. It involves verifying insurance, submitting accurate codes, and managing any claim denials to ensure steady revenue.